How to create a top-notch digital banking app

How do you create a digital banking app that stands out on the market? Here are the steps to take to build a top-notch digital banking app.

Managing your finances is often challenging. Job loss, the global pandemic, or even something as simple as the temptation to buy the latest iPhone can derail even the best-laid financial plans.

No wonder, then, that personal finance apps are on the rise. These platforms promise to ensure users have a better grasp on their money through the power of technology.

If you’re looking to get into the fintech space, personal finance apps are a fantastic entry point.

Interested? Here’s how to build one.

Start by brainstorming the list of features you want for your personal finance app. No doubt this process will be a challenge in its own right, because there are so many options available.

Luckily, you’ll find plenty of inspiration from successful apps already in the market, such as Mint and Albert.

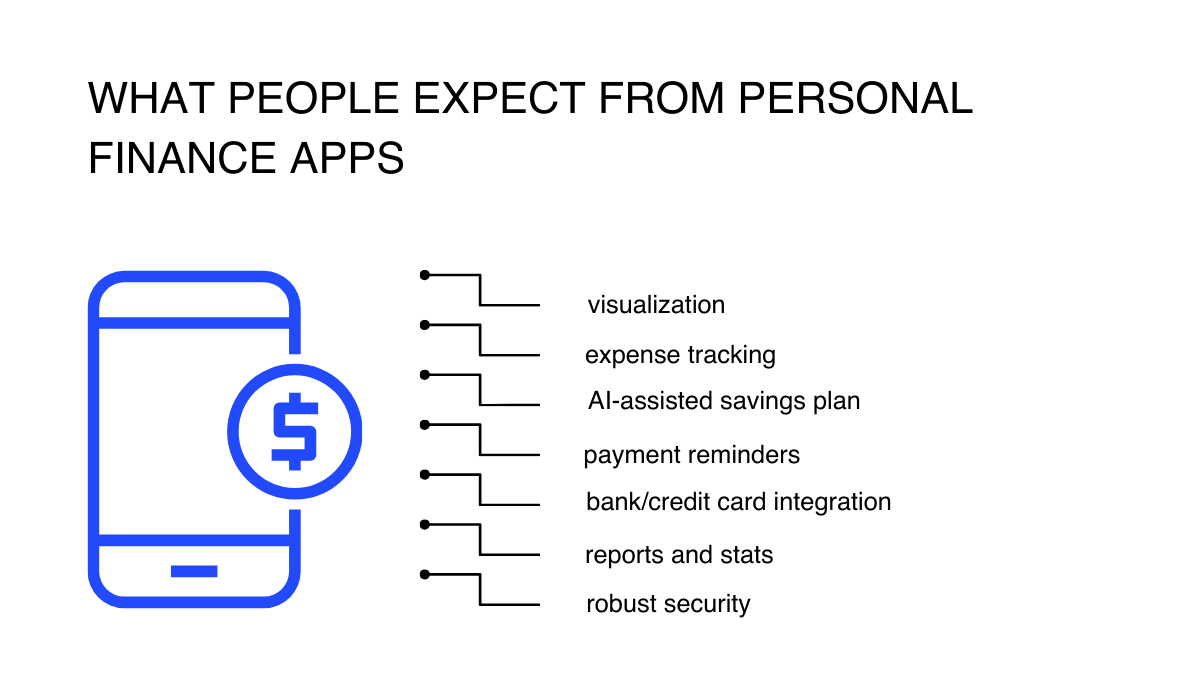

Keep in mind that users expect their finance app to have certain fundamental features, such as:

Source: DECODE

Every one of these components contributes to your app’s overall usability.

Visualization, for instance, helps present finances in a way users can easily understand. On the other hand, payment reminders help a person reach their savings goals by ensuring they don’t miss their key financial obligations.

Next, to further narrow down the features to focus on, you should pick the type of personal finance app you want to create.

Major businesses trust us to handle their mobile banking solutions, and we help agile startups disrupt mobile payments, stock trading and the rest of the rapidly evolving sector.

For example, budget planners are the most basic apps you can make. They allow users to track expenses and set limits based on a predetermined financial goal.

Habit tracker apps take it a step further by using AI to analyze your spending habits and suggest a savings plan that best suits it.

You can also focus on investment apps that help users compound their extra money through stocks, bonds, P2P lending, and other financial instruments.

But you should go beyond the fundamentals. Introducing innovative features or even putting a new twist on budgeting will make your app stand out.

One good example is the YNAB (You Need a Budget) app and their Four Rules method:

Source: DECODE

Lastly, consider conducting interviews or feasibility studies to better picture your target market’s pain points, so you can devise app features that fit their exact needs.

Personal finance apps tend to connect with financial institutions and other fintech apps, making them more convenient to their users.

Let’s say that your app needs to retrieve a user’s balance from their bank account. You could connect your interface with payment platforms like Paypal or Apple Pay so the user can make payments directly from your app.

Integrations are essential for finance apps because they streamline the process for your users, delivering a better user experience and encouraging the adoption of your app.

And if you’re still not convinced of the importance of integration, take a look at this research data:

Source: Mulesoft

As you can see, providing an integrated personal finance solution can help you win over that 57% over to your side of the fence.

Integrations are done using an Application Programming Interface (API). These act as the bridge that allows different platforms to communicate and exchange data.

Aside from making integrations possible, APIs also help speed up development since you don’t need to create different integration functions from scratch.

There’s an API for virtually every aspect of your personal finance app. Plaid, for instance, allows you to connect a user’s bank account to your app easily. If you want to enable payments, you can connect to the Stripe API.

You can even implement cross-border payments and currency conversions using APIs like Uphold.

However, with the myriad choices before you, it’s crucial that you plan which integration APIs you need to work with.

As with any fintech app, security should be at the top of your priority list. After all, we’re talking about people’s money and data here.

You also don’t need to look very far to realize that cyberattacks are rife in today’s interconnected world.

In the World Economic Forum’s 2021 Global Risk Report, cyberattacks came in 4th place as one of the gravest threats facing the world in the coming years.

When do respondeds forecast risks will become a critical threat to the world?

Source: World Economic Forum

Financial apps are especially at risk, since hackers will exploit any vulnerability to gain direct access to the users’ money.

For instance, most apps work in a client-server architecture, meaning the relevant data is constantly transmitted to and from the app. Without adequate safeguards, hackers can easily intercept the data stream and steal sensitive information.

Fortunately, there are plenty of ways to make your app security airtight.

Here’s a quick checklist, courtesy of MobiWeb:

Source: DECODE

Incorporating biometrics and two-factor authentication (2FA) to verify logins and transactions are also fundamental steps in guaranteeing security.

These two protocols can stop most hacks like phishing and brute force attacks. They can also protect a user’s data if they lose their phone.

Encrypting user data using standards like AES and PGP is also paramount. This guarantees that, even if hackers do get hold of it, any data they gain access to will be unusable.

It also helps you become more compliant with data protection standards such as the GLBA, GDPR, and PCI DSS.

Other best practices include thoroughly vetting third-party libraries, automatically logging off after a short period, and boosting server security through firewalls and anti-virus software.

Finally, don’t forget about educating your own team and employees because, according to Kaspersky:

“We’ve found that just over half of businesses (52%) believe they are at risk from within.”

Because cyberattacks are so prevalent, you have to do everything in your power to protect your clients’ data.

Once you have a rough idea of your personal finance app’s features, integrations, and security layers, it’s time to figure out the tools you’ll need to bring them to life. This is referred to as your tech stack.

Your first decision is to choose your preferred programming language.

For reference, here are the top picks for fintech projects worldwide as of 2020:

Source: The Codest

Python is a popular choice for a reason. It’s fast, simple, and easy to learn, which is beneficial for bringing fintech apps to market faster.

Error rates and bugs are also lower. But despite the simplicity, Python is a robust language with good security and plenty of libraries specifically for financial applications.

Java has been used for decades in enterprise and financial software, making it a good candidate for fintech. And the reason for this is Java’s tight security and OS independence, which means it can be coded once and deployed anywhere.

The only problem with Java is that it tends to be slower and more memory-intensive than Python.

Next, C++ is a powerful classic language that also sees use in fintech. Its greatest strength is its execution speed, which makes it fantastic for apps requiring complex financial calculations. However, C++ can be difficult to learn.

Aside from these core languages, you should also consider the language you’ll use to develop the app itself. This decision will largely be made for you the moment you choose to go either native or cross-platform.

For more information on mobile app programming languages, you can read our excellent guide here.

Here are some essential questions to help you flesh it out further:

In the end, either of the tech stacks we’ve described can help you build a great fintech app. What you eventually choose will depend on your project’s scope and goals.

An exceptional user experience (UX) is something that every personal finance app needs to succeed. Remember, you’re trying to make managing finances easy for your users, and the look and feel of your app have to match that.

A simple user interface (UI) is key to achieving a satisfying UX. It must achieve a balance of simplicity and attractiveness. For instance, while a beautiful font might be great from a design standpoint, it’s useless in a finance app if it’s hard to read.

Good flow from one screen to the next is also paramount, as users can easily get overwhelmed with lots of financial data. Consider only showing the information the moment it’s needed. And to truly ensure usability, proper onboarding is non-negotiable.

Source: Career Foundry

One point worth mentioning is that you should always use simple language and avoid jargon in your app. This ensures that everyone, regardless of financial knowledge, can understand what’s happening on-screen.

In addition, this helps give your app more transparency, which is crucial for gaining users’ trust.

In line with this, it’s also essential to keep accessibility in mind when designing your UX. Relying on inclusive design principles will widen your app’s reach, appeal, and even revenue.

And the segment of people with disabilities is a force to be reckoned with—seeing as they spend half a trillion dollars annually.

However, while ease of use is the core goal of UX design, it shouldn’t be too easy to complete certain actions in your app. There should still be some amount of friction, as noted by a Usability Geek case study on Acorns and Venmo.

The reason? It ensures that users don’t easily make critical mistakes.

In the case of Venmo, it was as simple as adding an extra confirmatory step when a user is about to send money. This guarantees that the user is aware of the transaction and that he or she is OK with doing it.

These UX tips are just the tip of the iceberg.

Indeed, there’s a lot that goes into creating a UX-optimized, user-friendly app. If you’d like to know more about the topic, check out our handy guide here.

Building a Minimum Viable Product (or MVP) is becoming an indispensable step in creating successful apps. And it’s becoming increasingly important in a saturated market with a growing number of competitors.

An MVP is necessary to validate your app in the real world. With it, you avoid wasting money developing an app that turns out to have features that your market doesn’t want or need.

And with development costs averaging almost $300,000, an MVP can single-handedly spell the difference between success and failure.

With that, there are certain things an MVP should have for it to be effective:

Source: Daily Scrawl

The most important one is summed up in the word minimum, which means it should have just the core features—enough to attract users and investors to your app. Why? Because you want to develop an MVP as fast as you can.

As a rule of thumb, the process should only take ten months, at most. Anything longer, and you’re already beating the purpose of an MVP.

But at the same time, you want the app to feel as close to a finished product as possible, and not just a rough draft. Achieving this means not ignoring key app development phases like market research and testing.

It’s this delicate balance of speed and quality that makes MVP development quite a challenge. But the potential time, money, and effort you’ll avoid wasting will make creating MVPs worthwhile.

You need to test your personal finance app thoroughly, more so than any other kind.

The reason is obvious—you’re dealing with people’s money, so the potential consequences of neglecting to do so are catastrophic.

The testing you’ll do with a personal finance app is the same with any other kind of project, only much more rigorous.

Source: TestingXperts on Quora.com

These include both manual and automatic versions of functional testing, performance, and usability testing. Security is, of course, a top priority, so you’ll need to subject your app to a battery of penetration testing.

Since standard testing procedures might not suffice, given the sensitive nature of financial apps, testing with a cross-functional team is highly beneficial.

What’s a cross-functional team? It’s one that’s composed of individuals with different backgrounds and skillsets.

This illustration from Digital AI sums it best:

Source: Digital.ai

Why is this important in fintech testing? The fact is, most developers aren’t versed in finance. And this is a considerable risk since a small error or misinterpretation can cause untold losses. Hence, you need finance-savvy individuals involved during testing.

Integration with financial institutions and other sources can also complicate testing for personal finance apps since testers need to consider every scenario.

Another challenge is to optimize performance and guarantee zero slowdowns since users expect 24/7 access to their finances.

Once your app is finalized and nearing completion, it’s time to consider launching it. Keep in mind that there is more to making a launch successful than just publishing it on the Apple App Store or Google Play.

At its core, launching an app is simply marketing it to your target users. However, your goal is not just to get downloads but to have users continue using your app. This is called a retention rate, and it’s notoriously hard to maintain.

A quick look at this Statista research confirms this:

On day 1 and day 30 of mobile app installs worldwide as of August 2020, by category

As you can see, traditional banking, the fintech category with the highest rates, only achieved a 30-day retention rate of 13.4%. This means that, after a month, 86.6% of users uninstalled or stopped using their banking app.

Having a stellar app experience is key to keeping retention rates up. However, a good launch can do wonders as well.

Consider promoting your app like you would any other digital product. That means posting regularly on social media, creating SEO-optimized content to drive traffic, and investing in paid ads.

Don’t forget to have a conversion-focused landing page as well to improve your download rate further.

Creating an app demo video is also very effective when promoting a personal finance app. With it, you can easily show product features and demonstrate how easy it is to use.

Lastly, don’t forget to stick to App Store best practices to avoid being rejected. Nothing’s worse than putting in everything in your app’s launch, only to have it rejected by Apple or Google.

As you can see, there are numerous challenges you’ll face when creating your personal finance app. Nevertheless, the first and best step in facing it is always awareness. By knowing the pitfalls, you can prepare for them much better.

We hope our guide has inspired you to make your fintech app vision a reality.

And if you need help bringing that idea into the world, we’re more than happy to help! Contact us today to learn more.

Ante is a true expert. Another graduate from the Faculty of Electrical Engineering and Computing, he’s been a DECODEr from the very beginning. Ante is an experienced software engineer with an admirably wide knowledge of tech. But his superpower lies in iOS development, having gained valuable experience on projects in the fintech and telco industries. Ante is a man of many hobbies, but his top three are fishing, hunting, and again, fishing. He is also the state champ in curling, and represents Croatia on the national team. Impressive, right?

How do you create a digital banking app that stands out on the market? Here are the steps to take to build a top-notch digital banking app.

Fintech is a radical game-changer and beneficial for businesses everywhere, not just financial institutions.

Countless Fintech niches are popping up every day. The seven Fintech app types that we’ve described here are just the tip of the iceberg.