Fintech app security: what it takes to build a secure app

If you want to develop a fintech app, how do you protect your clients and their money? We discuss the most important considerations of fintech app security.

In many ways, fintech is one of the most unforgiving types of apps you’ll ever develop.

On top of the usual challenges of app development, it involves dealing with heightened security measures, complicated regulations, and tight competition.

Indeed, even a single mistake can bring down a fintech startup overnight, with massive financial and legal consequences. Just look at these ten app casualties for proof.

Nevertheless, while there’s a long list of fintech app pitfalls that can lead to failure, the ones we’re about to cover in this post are the most common, so they deserve your attention.

A great onboarding process can make or break any app. Teaching a person how to properly use your app turns them into a long-term user. It prevents churn, which is when a user abandons or (worse) uninstalls your app.

Your app’s churn rate is a crucial metric for app success, together with its opposite, the retention rate.

Unfortunately, keeping the churn rate low can be a considerable challenge, thanks to a saturated and rapidly evolving market.

Just take a look at Apptentive’s 2021 App Retention Benchmark report:

More than half of users abandon an app at the three-month mark.

App onboarding is essential for improving those numbers. Manish Kumar of the Natwest Banking Group summed it up best when he said:

“With very high churn rates for financial apps, onboarding experience and demonstrated value-based engagement are key to success in terms of user adoption.”

But for fintech, onboarding serves a much more vital role. Showing how your app works and how they can benefit from it helps build trust. Thus, when you need to collect their sensitive financial information, they are at ease while doing so.

Surprisingly, not many developers devote the time and attention necessary to do proper onboarding. According to a Wyzowl study, over 90% of users feel that most companies “could do better” when it comes to onboarding.

Part of the challenge is that proper onboarding is a balancing act. You don’t want it to be so short that it leaves users confused and uninformed.

But an overly extended onboarding process is harmful, too, as it adds unnecessary expenses and can bore the user.

A rule of thumb is that the more complex the app, the more involved the onboarding process tends to be.

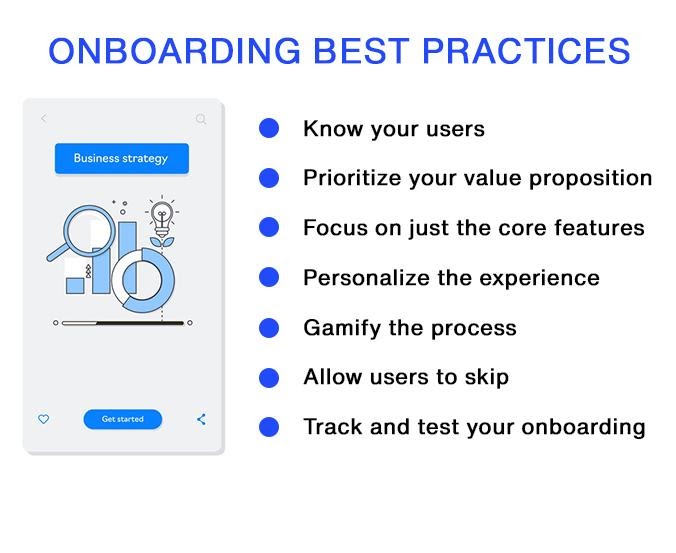

Here are some other app onboarding best practices to keep in mind:

Source: DECODE

But if you had to rely only on one guiding principle for onboarding, it’s this.

Help your users get comfortable using your app in the shortest amount of time possible.

Want to learn more about proper app onboarding in-depth? Check out our helpful guide here.

Many developers think that cramming an app with features is going to make it more appealing to the market. But, in reality, the exact opposite is true: having too many features actually detracts from a great user experience.

There are two big reasons for this.

The first one is that doing too much dilutes your focus.

Instead of perfecting a few essential features, you drain your resources developing many mediocre ones. And if the fundamentals of your app aren’t spot on, you risk losing users. According to Saleem Arshad of W1TTY:

“If the fundamental objective of the app is not met, it will cause a lot of frustration among users resulting in them moving to other apps.”

The second reason is that too many features can negatively affect your UX, as mentioned earlier.

If the app is too crowded, users will need to navigate countless irrelevant features to get to the function they need. This can bloat file sizes considerably and impact performance by slowing the app down, or worse, confuse users entirely.

So how do you know which features you should include and cut from your fintech app? It all depends on the needs of your target audience.

In other words: what is the big problem that your app is aiming to solve?

To figure this out, it pays to conduct proper market research:

Source: DECODE

Let’s say you’re trying to serve unbanked individuals with your app. These people would probably need just the basic services like savings and money transfers, so adding extras like investment options might only intimidate them.

Remember, people don’t care about your app. They only care about how it will solve their biggest problems. So if you only need one feature to do that, don’t complicate matters by adding more.

A poor user experience (UX) will make it very hard for your app to succeed, no matter how groundbreaking or revolutionary its features are. If people find it difficult, challenging, or even intimidating to use, they will churn.

Remember, many people already view financial services as complicated and confusing. So to succeed, your fintech app should be easy to use.

It is essential that the app flows from one screen to the next logically and seamlessly through an engaging user interface (UI). In the fintech niche, that means that, to prevent overwhelm, your app should only show financial data relevant at that exact moment.

Education and transparency are also vital but often overlooked aspects of excellent UX.

Using simple language and explaining important concepts will help widen your app’s reach and retention. At the same time, however, your UX should include some friction when making key transactions so that users don’t make critical mistakes easily.

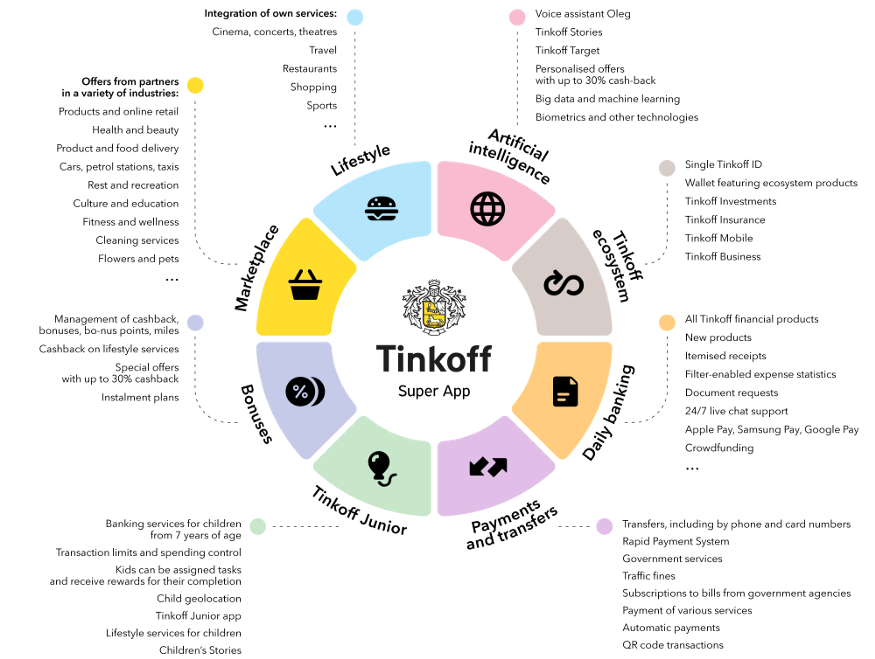

Recently, there has been a trend of boosting UX through the use of AI and machine learning. To help illustrate this trend, let’s look at super apps.

The concept of a super app was first defined by the founder of Blackberry, Mike Lazaridis, who described it as: “a closed ecosystem of many apps that people would use every day because they offer such a seamless, integrated, contextualized and efficient experience.”

To give you an example, in 2019, the Russian bank Tinkoff launched a banking super app that included a slew of services from financial to travel.

Here’s an overview of their ecosystem:

Source: Tinkoff

At first glance, this might seem to violate the rule that an app should have only essential features.

But the reason we’ve included this example is that it illustrates the power of a fantastic UX.

Tinkoff’s app works because it uses AI to show only the relevant features to the user, thereby avoiding overwhelming them.

In the end, great UX is more than just a smooth UI or jargon-free descriptions. It’s all about delivering meaningful and relevant experiences to your users.

Poor security will instantly spell doom for any fintech app. After all, you’re dealing with people’s hard-earned money and sensitive financial information here. Even one hack would compromise your reputation beyond repair.

The big challenge with app security is that you need to deal with constantly evolving threats, both internally and externally:

It also doesn’t help that the financial sector is the favorite target of hackers and cybercriminals, according to a Mastercard report. In spite of this, close to 98% of fintech apps lack sufficient protection from such breaches.

Realizing security mistakes is the easy part. Fixing them is much more challenging. Fortunately, you have many well-known best practices and tools at your disposal.

The first step is ensuring the security of your app, with flawless app logic, secure coding practices, and multiple layers of user authentication and authorization.

However, focusing on the app itself is not enough. You should go beyond and strengthen the ecosystem it’s in.

That includes your network infrastructure, databases, and web servers.

In fact, keeping them safe is paramount as they provide more attack surfaces that hackers can exploit.

You should also pay close attention to your app’s connections to third-party platforms and APIs.

Insecure communication channels between these points can allow criminals to steal account information or enter your system.

In the end, cybersecurity is a never-ending game. Attacks are getting more frequent and sophisticated, and some estimates indicate these incidents are going to cost businesses a staggering $10.5 trillion by 2025.

Therefore, constant vigilance and implementation of the latest security practices are vital to helping you avoid losses.

Data cleansing involves correcting errors or inconsistencies in a particular data set. It’s a crucial step for many fintech apps that retrieve data from other platforms or financial institutions via APIs like open banking.

By default, any data coming from outside sources is considered “dirty.” Often, the various formats the data come in are incompatible with your app. You’ll also encounter quality issues, outdated information, or inaccuracies.

As a result, using dirty data as-is can give you inaccurate or unpredictable results.

Unfortunately, the process is often overlooked by app developers, leading to detrimental consequences.

For example, imagine if a user’s bank account read “$10,000” instead of “$1,000” due to a data import error. What would happen if they suddenly withdrew that $10,000? The resulting mess would be incredibly complicated and tedious to clean up.

Thus, you need to clean the data first to make it ready for analysis. Apart from making it standardized, you also ensure that every piece of data you work with is verified, complete, and error-free.

Data cleaning is a multi-stage process that involves several steps. These are as follows:

The main challenge with data cleaning is that it’s intensive and time-consuming, especially when working with thousands of data points. One solution is to use AI to augment some cleaning stages for faster execution.

However you want to do it, the bottom line is that data cleaning is critical for the proper functioning of many fintech apps.

Testing is, without a doubt, the foundation of a quality app. Without it, errors and bugs will continue undetected, leading to a poor user experience at best and critical failures at worst.

But you’d be surprised how many fintech startups compromise their testing so they can launch apps faster. This is an observation shared by Russel Luis E Fernandes of Trust Payments:

“Loads of financial services companies are keen to launch products at pace without doing the bare minimum — adequate testing.”

This can be an expensive mistake, according to the 1-10-100 quality principle. In a nutshell, the principle says that the cost of fixing errors grows by a factor of ten the later it is in the software development life cycle:

Fintech apps also need sufficient financial testing since they must comply with regulations and other quirks unique to the financial industry. But, unfortunately, most developers aren’t financial-savvy enough to do this adequately.

To avoid these problems, it’s best to adopt a continuous and thorough testing paradigm, such as the software testing life cycle (STLC).

This process integrates testing into every software development phase, from planning all the way to launch.

As a result, STLC helps you catch more bugs faster, enabling you to launch quality apps on time.

It’s also vital to have a cross-functional testing team composed of members from diverse backgrounds and specializations. The many different perspectives they offer can help you thoroughly test your fintech app on all aspects:

The bottom line is that you can never have a 100% error-free app on launch. But by employing continuous testing practices, you ensure that you catch the most critical errors that would otherwise lead to failure on time.

For more information on testing, check out our comprehensive articles on types of software testing and manual vs. automated testing.

Active monitoring is the process of tracking bugs, errors, and crash data from live app users. The immediate insights this gives can help developers fix critical issues and refine overall UX for future versions.

Unfortunately, not many developers utilize sufficient monitoring to their detriment. As a result, they take a long time to discover and react to bugs in their app. This timeframe is referred to as the mean time to resolve (MTTR) metric.

The longer the MTTR, the more havoc a bug can wreak. This eventually leads to users abandoning your app entirely.

The key to a shorter MTTR is to identify issues as quickly as possible, thus kickstarting the entire incident management process:

Active monitoring is an essential component of early identification. Even something as simple as an error log with relevant information can help you uncover bugs as they happen. Integrating real-time streaming can make discovery even faster.

If it’s your first time developing a fintech app, chances are you’ll make a few of these common mistakes. But as we said, even a tiny error can bring devastating consequences.

So, what do you do?

Your best option is to work with a mobile app developer like DECODE, which already has a few successful fintech apps on its roster. That way, you can benefit from our rich experience and knowledge to help you avoid the common fintech app pitfalls.

Interested in working with us? Contact us today, and let’s talk about your next big app idea!

Ante is a true expert. Another graduate from the Faculty of Electrical Engineering and Computing, he’s been a DECODEr from the very beginning. Ante is an experienced software engineer with an admirably wide knowledge of tech. But his superpower lies in iOS development, having gained valuable experience on projects in the fintech and telco industries. Ante is a man of many hobbies, but his top three are fishing, hunting, and again, fishing. He is also the state champ in curling, and represents Croatia on the national team. Impressive, right?

If you want to develop a fintech app, how do you protect your clients and their money? We discuss the most important considerations of fintech app security.

So before going any further with your Fintech project, here are seven things you have to consider first.

Thanks to social distancing and lockdowns, FinTech apps are becoming indispensable in everyday lives. Here are the main steps towards building a FinTech app.