Top 13 fintech trends for 2021 and beyond

We’ve covered some of the biggest and most exciting trends in the FinTech world.

If there’s one industry that came out on top during the COVID-19 pandemic, it’s Fintech.

As of 2021, there are over 26,000 Fintech startups worldwide. Even more impressive is that the number of firms was only 12,131 in 2018 and 12,211 in 2019.

That means Fintech more than doubled in growth during the global health crisis.

That shows you how promising and resilient Fintech is and why it’s an exciting niche to get into right now.

But beyond the opportunities and profitable numbers, developing Fintech products today is actually a tall order. You’ll need to face confusing government regulations, development challenges, and a sea of competitors to bring your idea to market.

So before going any further with your Fintech project, here are seven things you have to consider first.

The first step in making any Fintech product is to decide on the niche. And if you’re new to the scene, you’ll be surprised to know that there are dozens to choose from.

To give you an idea, here are some you can explore right now.

Platforms that enabled users to transfer money online or make contactless purchases were extremely popular during the COVID-19 pandemic for obvious reasons. This is one area of Fintech where tech giants like Apple, Google, and Amazon love to play.

Helping people manage their money better is one of the most common applications of Fintech.

The emergence of AI automation, open banking, and API integration has made it easier than ever to centralize a person’s finances, making this a good niche to get into.

Gone are the days when trading was solely in the realm of financial institutions and elite investors. Instead, fintech trading apps like Robinhood and eToro have democratized trading, enabling anyone to invest in any stock market in the world freely.

One of the latest financial sectors to be changed by Fintech is insurance. Called insurtech, this innovation uses AI and automation to help clients find the best policy at the best price.

Fintech can also help entrepreneurs and small businesses access financial services like accounting, lending, and payment processing.

This is especially critical in marginalized countries where many business owners are still unbanked.

The above items are just the tip of the iceberg. Underserved sectors and emerging trends will undoubtedly create more Fintech niches in the future.

Offering a little bit of everything might seem like a good approach at first glance. After all, that way, you get to cover the most number of users.

But being the “department store of financial services” is actually counterintuitive.

The reason?

There are far too many financial services and niches available for one startup to cover feasibly.

Even large financial institutions and banks that offer everything under the sun don’t do it right. In fact, filling these “gaps” left by banks is why most Fintech startups exist in the first place.

It’s much more profitable to pour all of your resources into a specific niche, increasing the quality of that offering and thus standing out from the crowd. Not to mention that development will be faster and maintenance easier since there are fewer features to deal with.

Major businesses trust us to handle their mobile banking solutions, and we help agile startups disrupt mobile payments, stock trading and the rest of the rapidly evolving sector.

Focusing on a specific niche has always been the secret of success for so many startups and companies.

Just look at Slack, a multibillion-dollar tech company that focuses only on a single niche—digital business communication.

Now that you know the benefits of narrowing down your niche, how do you go about picking one?

There are many approaches and factors to consider, but the most important one is finding a specific problem to solve. Every startup and innovation, Fintech included, is a solution to an existing market issue.

Maybe you recently had a bad experience with a bank transaction. That can inspire you to get into the mobile banking or payments niche to improve the status quo.

Personal advocacy can also be your motivation. Suppose your passion is in helping marginalized individuals or business owners.

In that case, you might get into the financial inclusion or lending niche.

However you choose your niche, the key with Fintech is to innovate. Pick an area where you believe you’ll have the best chance to make an impact on your audience.

But picking a niche isn’t enough. You also need to consider your target market.

Picking the location and country for your Fintech product will serve matters because it will impact every aspect of your project and further refine your offering.

The primary reason is that different countries have varying financial laws and regulations that you need to comply with. For instance, many countries still ban Bitcoin, while others have regulatory gray areas regarding cryptocurrencies.

Different countries will also have different levels of sophistication and market needs, which will dictate what types of Fintech innovations will work well there.

For example, if you plan to get into the financial inclusion niche, you’d do well to target marginalized or unbanked countries.

Likewise, an area with a low smartphone or Internet penetration will see very slow Fintech app adoption. The prevailing culture also plays a role.

With that said, it’s far easier to offer your product to countries that are already receptive to Fintech products. For example, the United Kingdom was the world’s Fintech hub in 2020, with over 20 Fintech startups and 47 licenses issued. Other Fintech destinations include the US, Spain, Switzerland, and Singapore.

Like picking a niche, zeroing in on your country of choice depends on several factors.

The most important is how knowledgeable and familiar you are with the location.

Living in the country you’ve chosen (or having someone in your team who does) is one of the best ways to gain deep insights into the problems and issues it’s facing.

Only then can you design a solution that’s a perfect fit for that area.

There’s also the level of competition of your chosen niche in the country. A saturated market can be challenging to enter, and you’ll need a stellar product and deep pockets to succeed.

Another critical factor is whether the area is even ready for your Fintech solution.

Knowing answers to these questions will let you determine if your product is profitable and scalable in that location.

The country’s economic stability, now and in the near future, also plays a significant role.

Ideally, you want to release your Fintech product in places with a stable currency, reliable banking system, and minimal to zero political unrest.

Lastly, there are the regulations you need to pass. Obtaining a permit to operate in a country unfamiliar with Fintech will be an uphill battle at best.

If you plan on going this route, be prepared to exert money, effort, and connections.

Regulations, in particular, deserve special mention and a large chunk of your attention. Here’s why.

Financial services and products are one of the most heavily regulated sectors in every country. So for your Fintech product to succeed, you need to comply with these issues successfully.

Regulations deal with many aspects of an app, such as cybersecurity, data protection, and management. But their purpose is the same—to help protect consumers from financial risk.

In a way, following regulations works to your benefit.

Offering compliant Fintech products means protecting your users’ data and shielding them from hacks and frauds. In the long run, this helps build your trustworthiness and credibility.

And in a sea of competing financial services and products, being ethical is the best way to earn consumers’ trust and stand out from the competition, according to Tae Wan Kim from Carnegie Mellon University.

Of course, the key reason to comply with regulations is that they can single-handedly bring you down if you don’t.

Fintech firms shut down by the Federal Trade Commission (FTC), such as Beam Financial are cautionary tales into what happens if you try to skirt around the rules.

Knowing which regulations apply to your startup is the first step on your road to compliance. These can vary, depending on your country and the nature of your product.

Let’s take the United States as an example since their regulatory agencies tend to be one of the most rigorous.

As your Fintech product will most likely target consumers, you’ll need to comply with consumer protection regulations set by the Federal Trade Commission (FTC). The agency mainly deals with fair business practices, privacy, and data protection.

A critical FTC regulation for Fintech is the Gramm-Leach Bliley Act (GLBA), which requires financial institutions to explain to consumers how their data is shared and protected.

Another is the Fair Credit Reporting Act (FCRA), a set of guidelines for companies collecting credit data.

In the European Union, one special consideration with data privacy is the General Data Protection Regulation (GDPR), which lays out data handling and privacy protection rules. This law applies to you as long as you store user data of EU citizens, even if you’re not operating in the EU.

Aside from consumer protection and data privacy, anti-money laundering regulations (AML) are also one of the more prominent laws you need to address.

In the US, AML is enforced by the Bank Secrecy Act of the US Treasury and the US Patriot Act.

If you offer cross-border transfers, this will be a crucial regulation to tackle.

Payment transactions, a critical function of many Fintech apps, are under the Electronic Fund Transfer Act (EFTA) of the Federal Reserve and Regulation E of the Consumer Financial Protection Bureau (CFPB).

Other regulations deal with specific situations.

Crowdfunding, for instance, is covered by the Jumpstart Our Business Startups (JOBS) Act.

In addition, initial coin offerings (ICO) are treated as securities and thus subject to regulations by the Securities and Exchange Commission (SEC).

In sum, compliance can be confusing, expensive, and messy to deal with—but the hard truth is that it has to be addressed one way or another.

Our advice is to start with your compliance process as soon as you can to get it out of the way.

The best approach here is to hire a lawyer with financial regulation experience in your chosen country. You can also use RegTech tools to help automate and streamline your compliance workflow.

Your competitive advantage is the thing that makes you stand out in the market.

It answers the fundamental question: why should consumers pick you over others?

Competitive advantage doesn’t necessarily mean something flashy or unique. At its core, it’s all about providing value to your users, the kind that your competitors can’t or won’t.

This is encapsulated in your unique value proposition (USP)—a statement that summarizes your competitive edge.

Knowing your competitive advantage is vital because you can’t market your product successfully without it.

This is especially true if you want to stand out in a market with big players.

You don’t even need to be the first to develop a feature or product to have a competitive advantage (chances are you won’t remain 100% unique for long anyway).

Just look at how Steve Jobs transformed Apple in 1997—a company with over 350 products but losing millions every quarter—into one of the most valuable tech companies in the world with the iPod and iPhone.

Note that these weren’t the first portable music players and smartphones—not by a long shot.

Instead, their competitive advantage was a stunning design, a ridiculously user-friendly interface, and a seamless device ecosystem.

Innovation is also how Fintech startups came about in the first place.

Their USP was often to look at gaps in the customer experience of big banks and develop apps that address them.

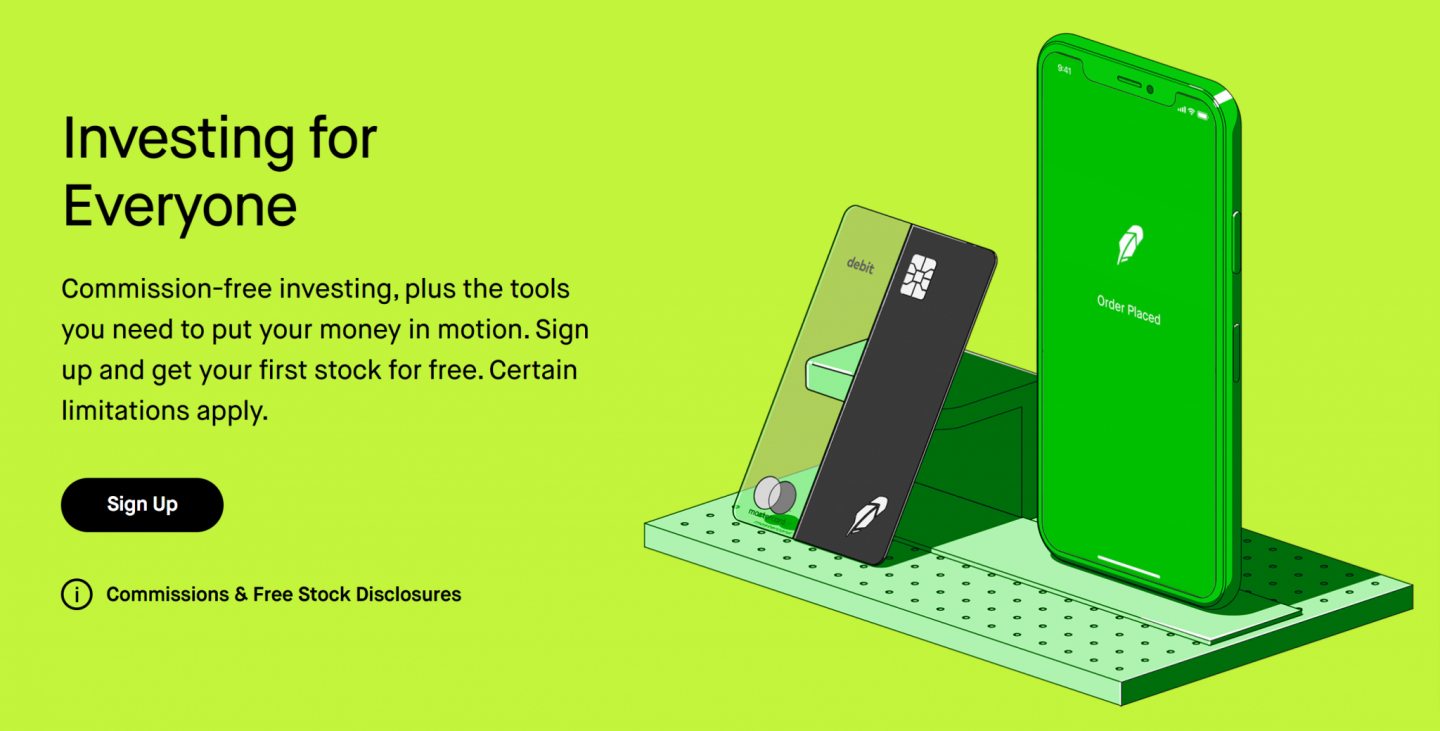

As an illustration, consider Robinhood’s USP: “Investing for Everyone.”

It’s an apt description of the app’s competitive advantage, commission-free investing, which no other financial company offered before them.

A competitive advantage can be anything. It can be a completely revolutionary idea, like Robinhood’s zero commissions.

Or, it can be an improvement over an existing feature, such as Stripe’s easy-to-setup and use online payment platform.

Even a fantastic customer experience can be a compelling advantage—something that Zappos is well-known for.

The quest for your competitive advantage starts with market research.

First, you should know your customers on a deep level and understand their problems, desires, pain points, and dreams. This allows you to brainstorm product features that will satisfy them.

The next step is competitor analysis, which is undoubtedly one of the most critical parts of your market research because it’s a goldmine of insights and information.

Look at your competitors’ products, strategies, and customer service. Find the gaps in their offer, then craft a product that will address those.

The final step is distilling your Fintech idea into a clear and concise USP.

Because while it’s tempting to address all of the problems and opportunities you encounter, tackling them all would be challenging and expensive.

So, pick just a few and refine your focus.

Unlike many other industries, the success of Fintech relies on integration rather than exclusion.

Therefore, you should consider the ways you can connect your app with other financial platforms, services, and tools.

To help you understand the trend behind third-party integration, consider that the average person tends to use multiple financial products.

You might, for example, access your account in your bank’s mobile app, transfer money with Paypal, and plan out your monthly budget via a planner like Mint.

Also, even though many Fintech startups are taking on the big banks, the reality is that Fintech as a whole still relies on them heavily.

Most people still have their money deposited in traditional savings accounts, so any Fintech app should allow users to transfer money (using Open Banking) between the app and these accounts.

Thus, it’s difficult and often rare for a Fintech app to exist in isolation because of the interconnected nature of the financial services industry.

Let’s cite a real-world example.

Molo is a UK digital mortgage platform that enables house buyers to choose a property, verify it with authorized agencies, and get an instant mortgage offer.

This is only possible because Molo integrates with other platforms, such as RightMove for real estate listings and Experian for credit scores.

Integration can also help speed up development time and lower costs because you don’t need to create everything from scratch.

Instead, your app can use existing APIs and third-party tools for standard yet crucial features.

For instance, there’s Authy for two-factor authentication (2FA) and Square for payment processing.

The modularity offered by third-party integration also makes swapping easy. For example, suppose the third-party tool you’re using isn’t working out anymore. In that case, you can simply exchange it for another without overhauling the entire app.

With third-party integration, you don’t need to reinvent the wheel. Instead, it’s smarter to use something that already works.

The technologies and tools you use matter in any software project, but they’re especially vital with Fintech, because of its sensitive and unique nature. Security, adaptability, and scalability are some of the minimum requirements of an effective Fintech tech stack.

However, with the various tools, programming languages, and platforms available, choosing the appropriate technologies to use in your Fintech product is always challenging.

So, how do you go about it?

Picking the right tech stack begins with knowing your project’s scope and goals.

Considerations like the feature set, the expected number of concurrent users, and whether you’ll collect customer data all dictate the technologies you’ll require.

Regulations will also impact your choice of tech stack more than you think.

For instance, AML regulations will require you to incorporate Know Your Customer (KYC) and other security protocols into your product, so you need to have the right tools to handle them.

Security is by far the most significant factor in a tech stack.

Vulnerabilities and security holes in your programming language of choice are all it takes to compromise your app. Third-party tools and software can also become weak links that hackers can exploit.

Let’s look over some tools and technologies commonly used in building Fintech products.

Python is arguably the most popular programming language in the Fintech space. Good performance, high scalability, a myriad of open source libraries, and an easy-to-use syntax make it suitable for rapid development and the MVP (minimum viable product) approach.

Java is the traditional language for enterprises and financial firms, which makes it a natural candidate for Fintech development. Excellent security and platform independence are what make it an ideal tech stack.

Finally, if your Fintech delves into complex computations and financial models, the native performance and concurrent operation of C++ is your best bet.

For mobile apps, you can use native tools like Swift or Kotlin. For hybrid or cross-platform development, you can consider React Native or Xamarin. We have discussed native and cross-platform app frameworks in more detail here.

Beyond the app itself, you should also look into server infrastructure on the backend, especially security.

Solutions like SSL certificates, tunneling protocols, and next-generation firewalls can help make your network environment robust against attacks.

SSL certificate is not a costly deal now. Either you purchase single domain, multi domain or wild card SSL certificate you will easily find cheap price along with strong encryption.

No matter which tech stack you choose, the important thing is that you opt for it because it matches your app’s vision, not because it’s the only one your development team is familiar with.

That’s why having an experienced and adaptable team is the most important asset you’ll ever have.

Even if you had the best Fintech idea in the world, backed by powerful technologies, all of that would fall flat without proper execution.

Hence, a savvy development team will spell the difference between the success and failure of your Fintech product.

But a typical developer wouldn’t cut it here.

That’s because Fintech includes financial aspects that a typical software developer isn’t usually exposed to.

It also has different system architectures, security standards, and protocols that require a whole new approach. Not to mention the endless regulations the programming needs to comply with.

And unlike vanilla app development, Fintech is an unforgiving niche where even the tiniest mistake can lead to expensive data breaches or, worse, a lawsuit.

There’s no shortage of cautionary tales in the industry, including the recent $600M hack of the cryptocurrency exchange site Poly Network.

That’s why the fastest way to ensure the success of your Fintech products is to get a development team with extensive experience building successful Fintech apps.

And that team happens to be us!

At DECODE, we’re proud of our expertise in building innovative Fintech apps with equally passionate firms.

One of them is the London SaaS company Bizzon, which partnered with DECODE to develop a seamless mobile ordering, payment, and operation management system for the hospitality industry.

Using our expertise in app development and low-level hardware implementation, we created a mobile app that can communicate directly with receipt printers and modules, essentially turning a mobile app into a POS device. The comprehensive solution also touched on purchasing, inventory management, reporting, and other critical business tasks.

Needless to say, the folks at Bizzon were impressed, especially with our in-depth expertise and analytical approach that went beyond the “norms” of software development.

Looking for something more serious and finance-heavy? We’ve done that too.

We partnered with the European Fintech provider Asseco SEE to work on a custom cross-platform mobile banking solution that included various financial services, from currency exchange to receipts management.

Working in a high-stakes sector with strict European data regulations presents enormous challenges, on top of the usual obstacles with software development.

But thanks to our in-depth knowledge and practical experience with PSD2 (the EU directive governing electronic payments), we were able to deliver a highly secure and compliant app.

We also utilized Open Banking architectures, robust security, and regular reporting with the Financial Conduct Authority (FCA).

The Bizzon and Asseco SEE case studies illustrate the high level of expertise and vision we bring to your Fintech project. Partner with the DECODE team and realize your idea’s true potential.

Building a Fintech app is no walk in the park. You have to deal with many unique problems, such as regulations and heightened data security, besides the standard development concerns like retention and user experience.

But with a structured approach, endless passion, and an experienced team, you can bring any Fintech idea to fruition.

Need assistance with your Fintech project? Contact us today, and let’s talk about how you can move forward.

Marko started DECODE with co-founders Peter and Mario, and a decade later, leads the company as CEO. His role is now almost entirely centred around business strategy, though his extensive background in software engineering makes sure he sees the future of the company from every angle. A graduate of the University of Zagreb’s Faculty of Electrical Engineering and Computing, he’s fascinated by the architecture of mobile apps and reactive programming, and a strong believer in life-long learning. Always ready for action. Or an impromptu skiing trip.

We’ve covered some of the biggest and most exciting trends in the FinTech world.

Thanks to social distancing and lockdowns, FinTech apps are becoming indispensable in everyday lives. Here are the main steps towards building a FinTech app.

Everything you need to know about 2021 fintech mobile app trends, opportunities, and regulations in this exciting time for personal finance innovation