17 mobile app ideas for startups in fintech

It’s no secret that fintech is now one of the hottest sectors to get into.

Thanks to the COVID pandemic, the adoption of digital financial services has only accelerated. And entrepreneurs are responding, with 2021 seeing a record-breaking 151 new fintech unicorns.

By 2022, the global fintech market is estimated to reach over $300 billion.

As a developer, getting into the action can be highly lucrative.

But where do you start?

That can be difficult to decide, because “fintech” is a very broad category. Under it are dozens of niches that touch on various services from loans to investments.

If you need a little inspiration, here are some app ideas you can explore.

Digital banking app

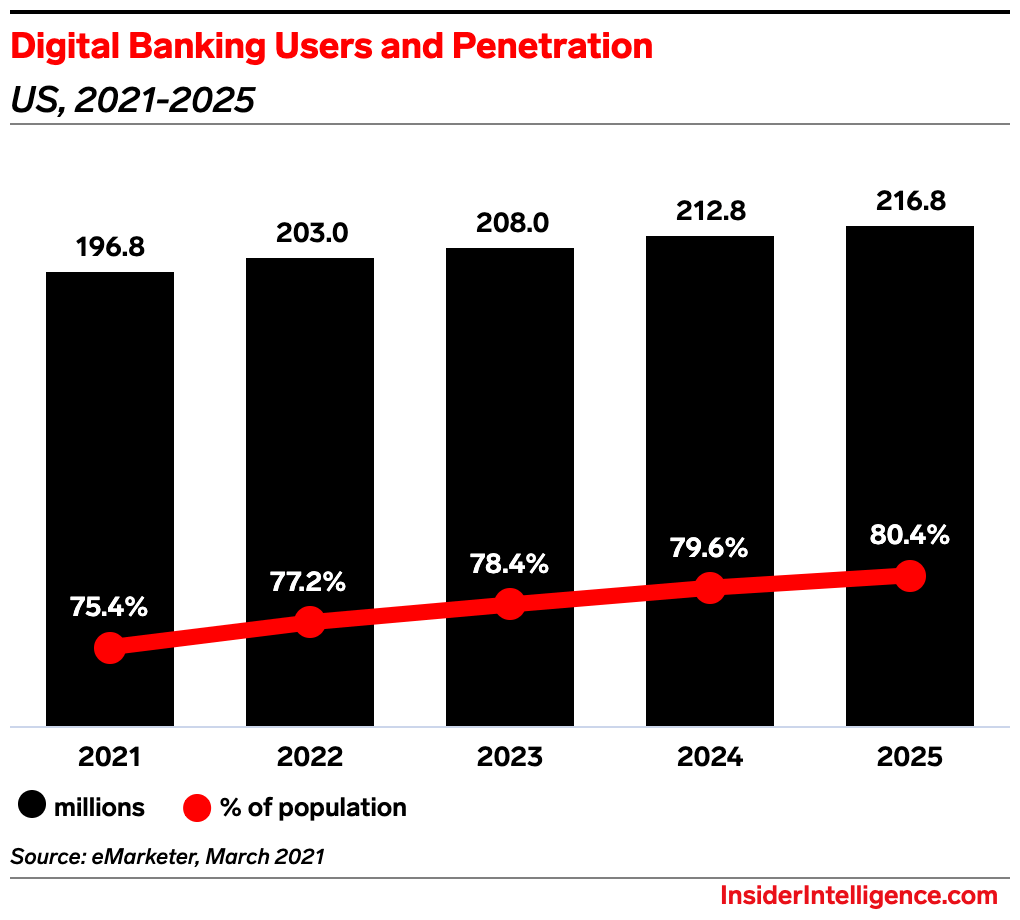

If there’s one niche that best exemplifies the possibilities of fintech, it’s digital banking. In fact, the industry was born out of the desire of challenger banks to offer a better alternative to larger financial institutions.

Due to the COVID-19 pandemic, people have seen the need for a digital way to manage their finances while stuck at home.

As a result, digital banking adoption continues to increase steadily and could cover 80.4% of the U.S. population by 2025, according to a study by Insider Intelligence.

Source: Insider Intelligence

The same study found that 89% of consumers use digital banking, with 70% stating it’s their primary way of managing their funds.

While digital banking can be a profitable niche, it is also highly competitive, full of players from both startups and established banks. So a key strategy here is to differentiate yourself with technology or even partner with a big bank.

Peer-to-peer payment app

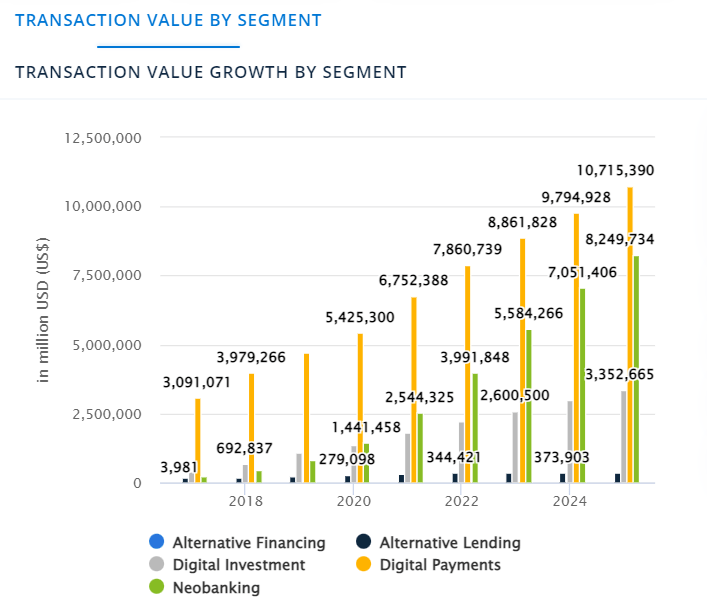

The digital payments niche is one of the most profitable ones to get into, boasting the highest transaction volume of any fintech category by a mile:

Source: Statista

Peer-to-peer payment solutions like Paypal and Venmo are among the most popular types of apps in this niche. They allow users to send and receive funds straight to their bank account with a few simple swipes on their smartphones.

Like digital banking, the peer-to-peer payment market can be competitive. Your app needs to be robust and secure to even have a chance. But at the same time, it also needs to be easy to use.

For example, all you need to send money on Venmo is the recipient’s username, email, or phone number. There’s no need for hard-to-remember details like bank accounts or credit cards.

Just remember to balance the ease of use with a little friction to prevent users from making critical mistakes.

Personal finance management app

It’s safe to say that most people are either bad at finances or hate them. Indeed, a Capital One survey revealed that managing money is the number one stress factor for 73% of Americans.

That’s why personal finance management apps are so popular. They provide a way for people to take charge of their finances with minimal hassle.

Because of this, these apps could become a permanent fixture in the user’s life, which can do wonders for your retention rate.

The popularity of personal finance apps is also rising: by 2027, the market will reach $1.576 billion.

Personal finance apps constitute a broad category, and there are a variety of subcategories you can choose to focus on.

For example, the popular app Mint handles investments on top of expense tracking. In contrast, You Need a Budget (YNAB) focuses more on budgeting.

For more info on creating a great personal finance app, check out our article here.

Investment app

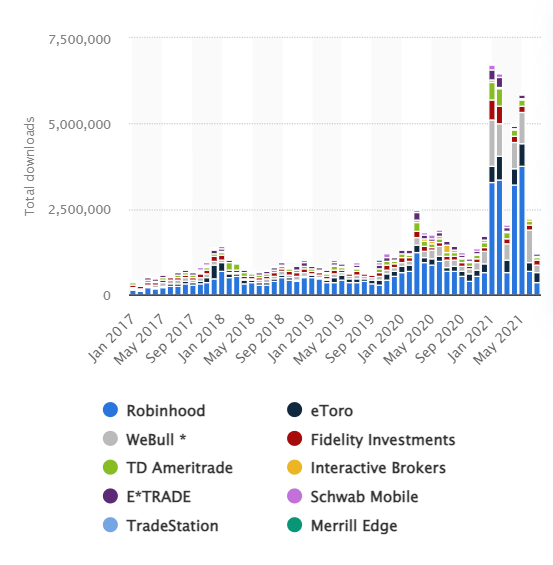

The meteoric rise of Robinhood has opened up the power of investing to everyday users and, with it, the popularity of investment apps.

Check out the sharp jump in app downloads during the pandemic:

Source: Statista

Investing is something that many people aspire to do but might not have the knowledge for. However, apps make investing more accessible, so you’ll always have a potential market.

There are many different ways to approach your investment app.

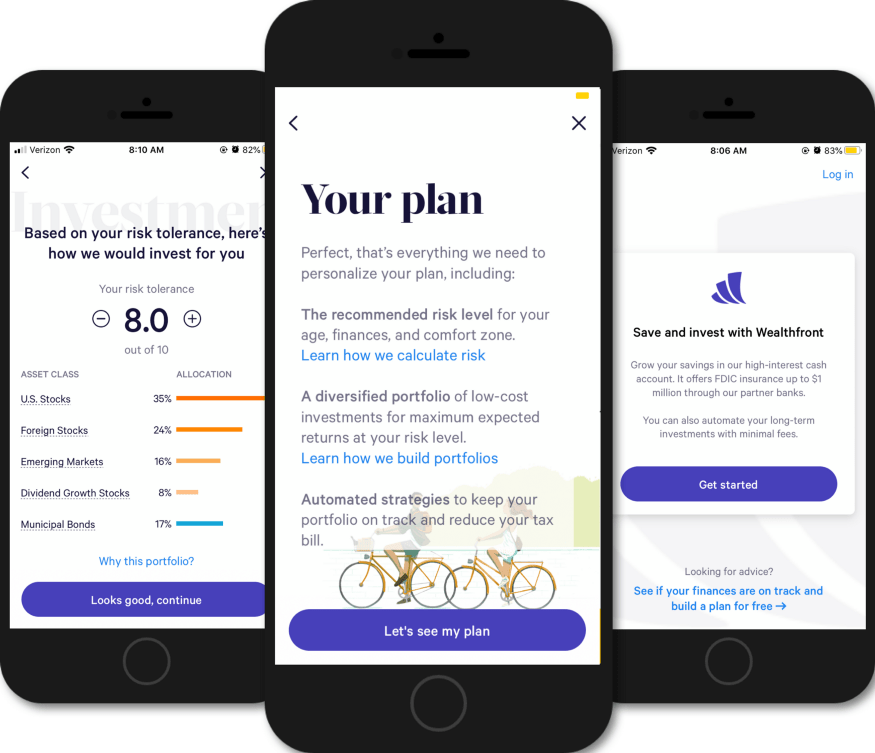

You can choose to cater to beginners or people who don’t want to manage their portfolios actively. In those cases, your solutions take on a role akin to advisory services, helping users navigate the best financial instruments to reach their goals.

One of the best examples of this is the Wealthfront app. It automatically curates the best investments for you based on a specific income goal and timeline.

Source: Slater Katz

On the other end of the spectrum, there are apps, like T.D. Ameritrade Mobile, which give savvier investors the power to make any trade they want.

There are also other subcategories worth exploring, like robo advisors and crypto trading apps. We’ll tackle those a bit later.

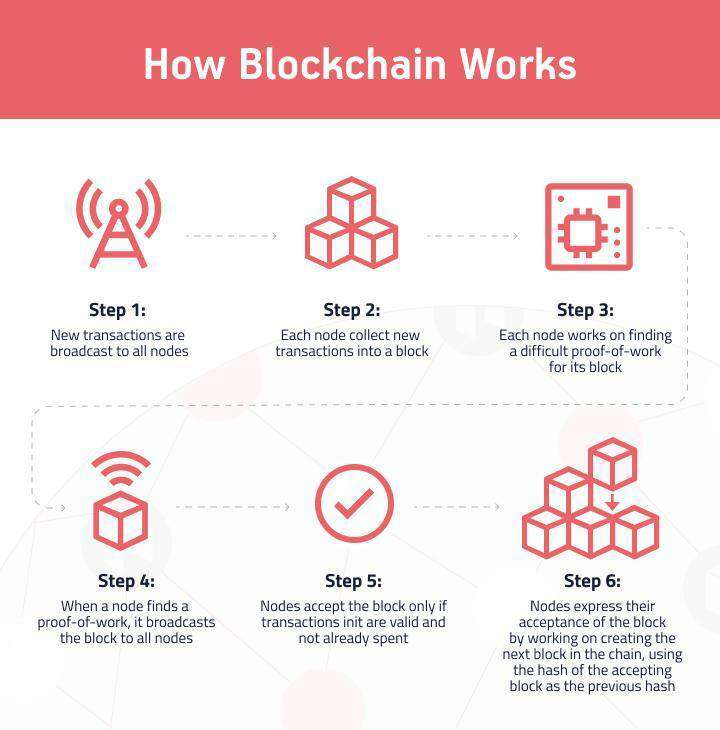

Blockchain app

Unlike others on this list, blockchain apps don’t describe what the app does. Instead, the term refers to the technology at its core—blockchain. In practice, this technology can be used in various industries and applications.

For example, blockchain games like Axie Infinity are becoming popular because they allow users to own and sell in-game assets.

Blockchain technology can also enhance business processes like logistics and supply chain management, such as the IBM Blockchain.

The common denominator of all these examples is the use of blockchain to decentralize processing. This makes the app highly secure and anonymous yet transparent.

Source: Mobindustry

There are also many ways to implement blockchain in your app. Building one from scratch is the most flexible option but also technically challenging.

Using readily-available solutions like Ethereum or a Blockchain-as-a-Service (BaaS) platform is an easier alternative.

Indeed, blockchain is one of the most exciting and innovative fintech niches. So if you have bold ideas or want to be on the cutting edge of fintech development, you’ll feel right at home.

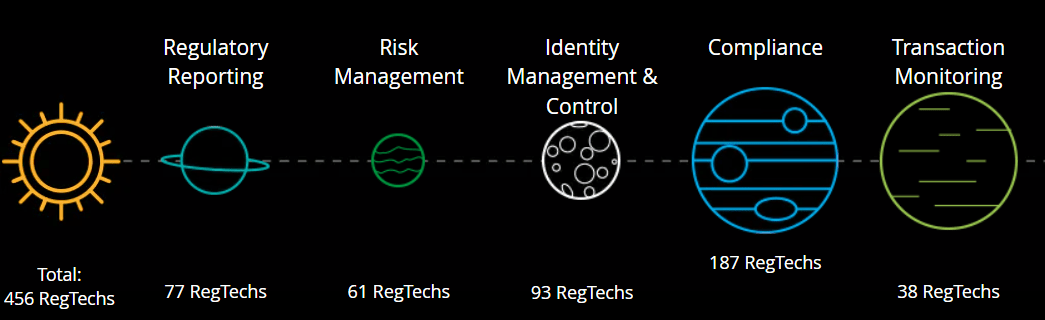

Regtech app

Regulatory technology (RegTech) is an emerging fintech niche that helps financial firms and institutions stay compliant. It plays a supporting, albeit important, role in the fintech ecosystem.

Regtech uses a combination of artificial intelligence and big data to spot irregularities in a firm’s operations automatically. This lessens the risks of money laundering, fraud, and other criminal activities.

With cybercrime getting increasingly regular and expensive, the demand for regulatory technology will only grow. The niche currently has around 456 firms working on various regulatory services, from transaction monitoring to identity control.

Source: Deloitte

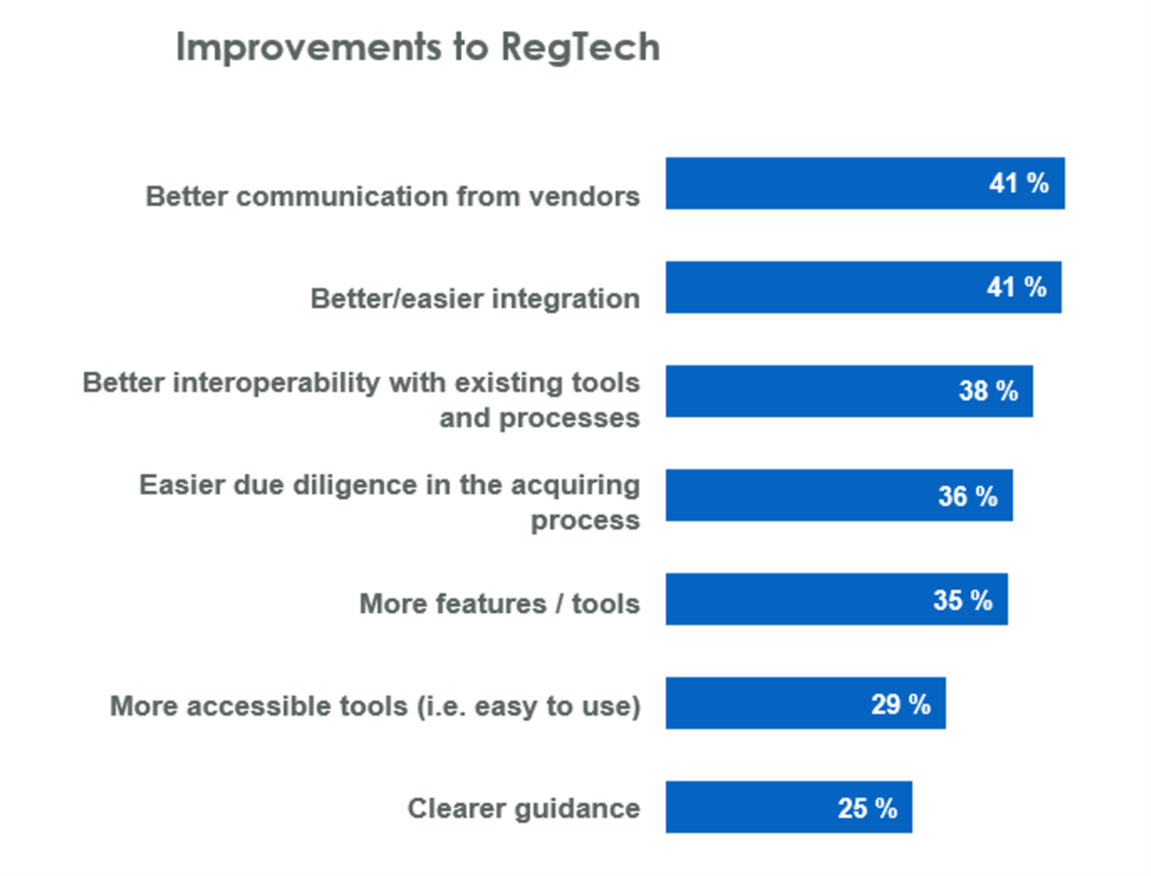

The good news is that while RegTech is already well established, there’s still plenty of room for growth.

Here’s a recent survey that reveals what firms want from their RegTech solution:

Source: FCA.org

Their preferences can be summed up as better communication and increased flexibility.

There are also other exciting trends in the niche, such as biometrics for AML initiatives (anti-money laundering) and more robust KYC (know your customer) verification.

That means RegTech should be a viable fintech niche for the foreseeable future.

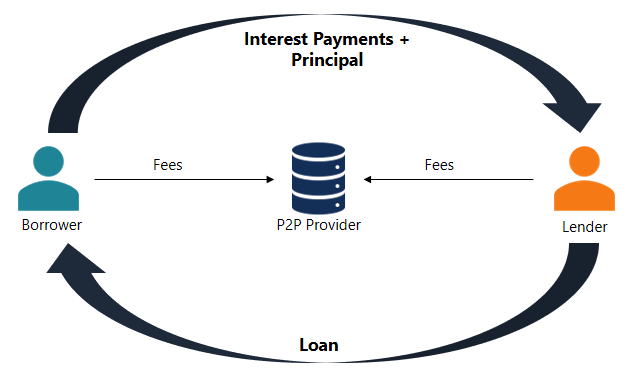

Loan lending app

Lending is one of the areas of finance that fintech has affected the most. Everyone knows how tedious and time-consuming it is to get a loan.

So, the solution was to connect borrowers and lenders directly for faster transactions.

One of the best versions of this is the peer-to-peer (P2P) lending app. Instead of a bank, borrowers are connected to other app users who have spare cash they want to invest and earn interest from.

Source: Corporate Finance Institute

Lending apps also make the process much fairer to both the borrower and the lender.

Using big data and integrations, the lender can get a much more thorough and accurate view of a person’s creditworthiness. This allows them to offer loan terms that are fair to both parties.

Aside from P2P, there’s also another type of lending that’s gaining popularity: payday loans.

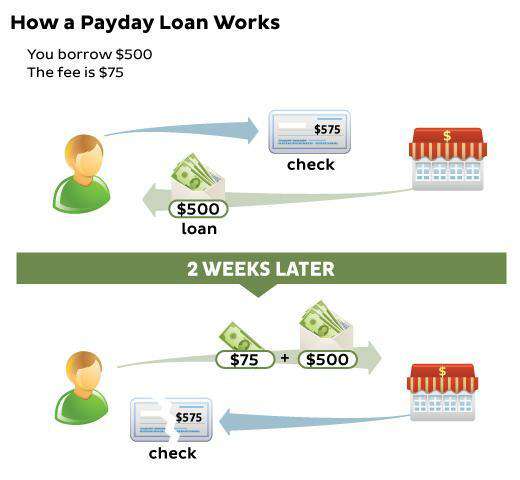

Payday loan app

Like any other lending app, payday loan apps allow you to borrow money at interest.

However, the difference here is that the lender will automatically deduct the loan payments from your paycheck.

Source: Consumer.gov

While convenient and readily accessible, the main disadvantage of payday loans is that they’re very expensive. They have nearly double the interest rates compared to personal loans.

They’re also riskier since they’re susceptible to predatory lending practices.

Fintech revolutionizes this practice by eliminating the interest rate altogether (although there are still some minimal fees). In addition, it also makes the process easy and intuitive.

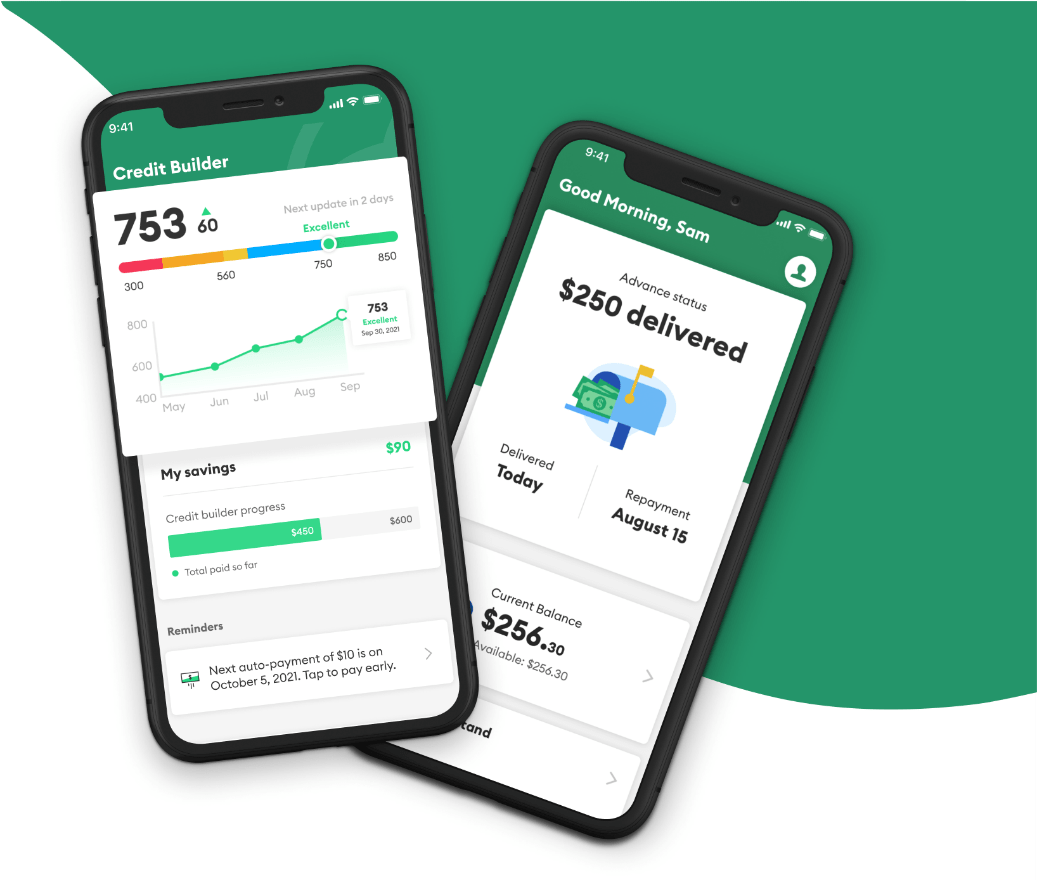

A great example of this is Brigit. The app allows users to borrow up to $250 with no credit check or collateral. It then automatically deducts the loan installment from your paycheck. Users can also extend their due date with no late fees.

Source: Brigit

Indeed, there’s still much space in this niche for more players and innovators, so developing a unique loan app might be a good option to take.

Buying insurance app

Buying insurance can be a tedious, even mysterious, process for many people. That’s why insurtech (insurance tech) apps are gaining popularity right now.

Insurtech provides insurers with a much more accurate way to assess a policyholder’s risk, so that they can offer fairer coverage. On the other hand, the insured can use insurtech to process claims faster.

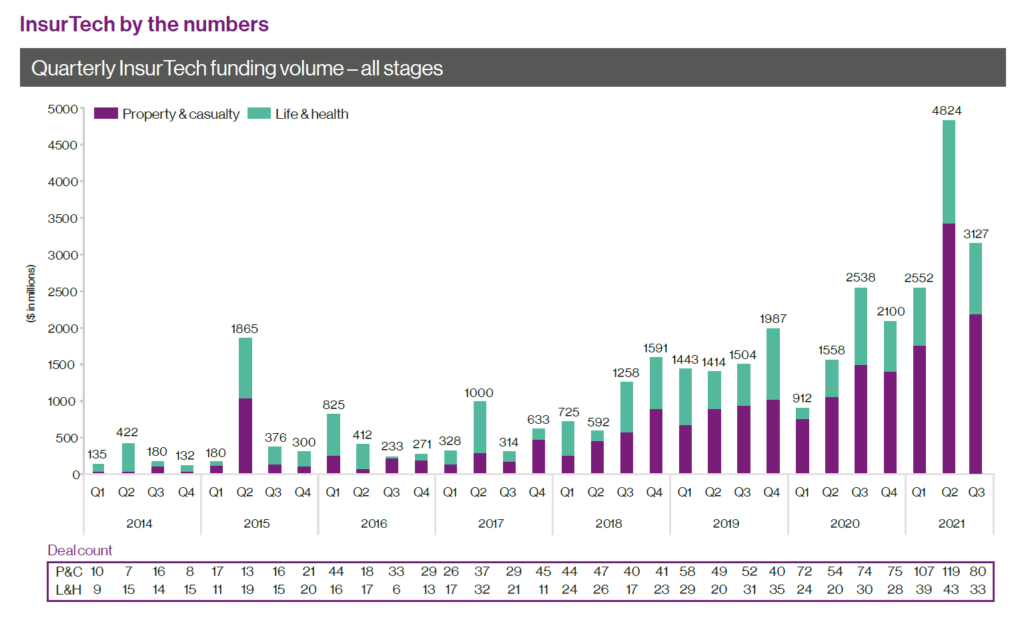

Insurtech is a rapidly growing market, with funding volume at an all-time high in 2021. That makes it a relatively attractive new niche to get into.

Source: CBInsights

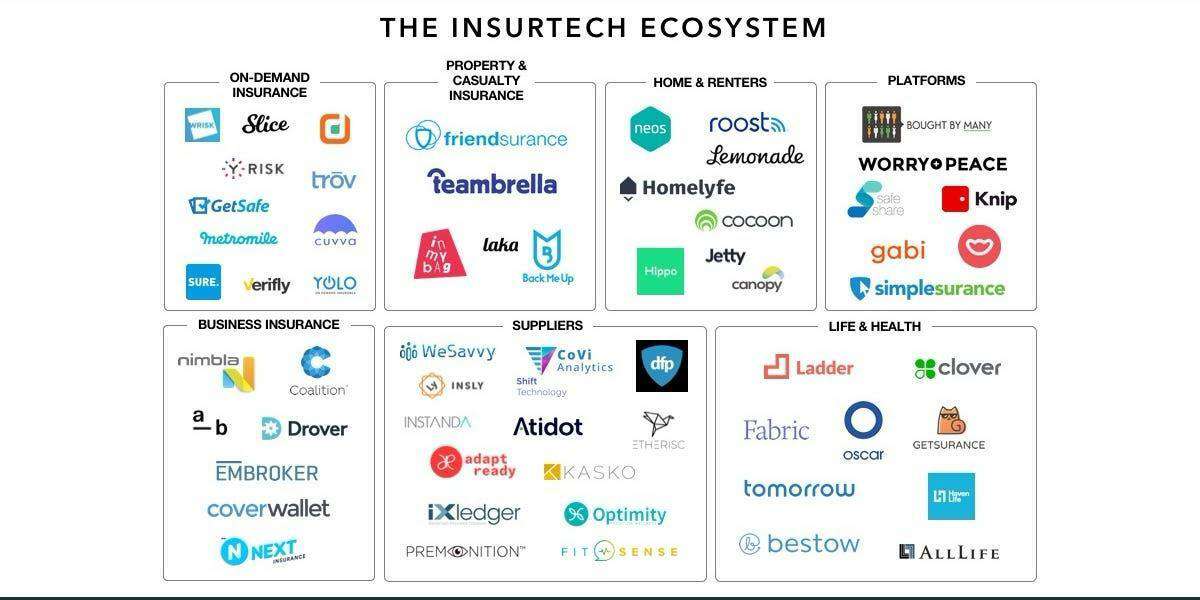

Your app can serve plenty of areas, should you go with this niche. For example, you can focus on home insurance, as the Lemonade app does.

Car insurance is also an in-demand niche, served by the likes of Root. Or you can be like Esurance and provide a wide range of services in the field.

Source: Business Insider

The wide variety of underserved sectors helps make insurtech an attractive option for developers.

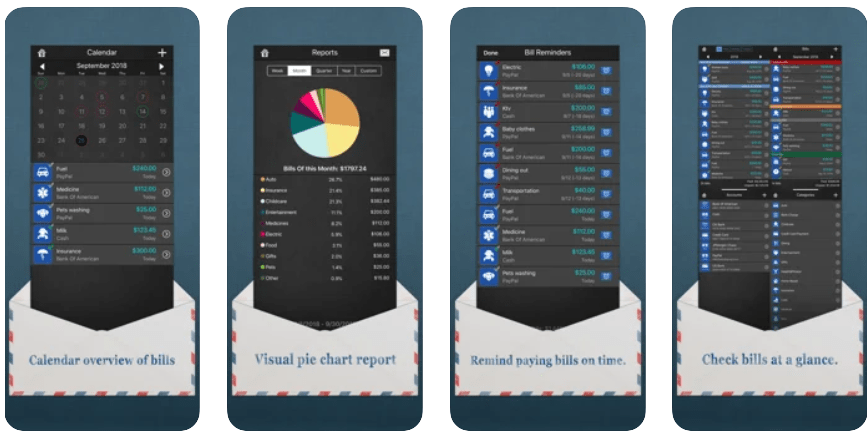

Bill reminder app

Bill reminder apps are usually a subcategory of personal finance apps since most offer a payment reminder feature.

However, it’s also possible to build an app purely for reminding people of their bills. So it’s a good route to take if you want to develop something useful but don’t want to deal with the complexities of building a personal finance app.

A good example of this app is Bills Monitor Pro. What sets it apart is that it allows you to get in-depth with managing your bills.

You get robust reminders, analytics tools, and various categories to organize your bills.

Source: Bills Monitor Pro app page

While simple, bill reminder apps can still be a valuable part of your user’s financial life if you play your cards right.

Alternatively, you can also use an app like that as a foundation from which you can eventually build an entire personal finance app.

Crowdfunding app

Crowdfunding is a method of raising capital by getting large numbers of people to invest small amounts of money in your venture.

It’s a great path for people who can’t qualify or afford traditional financing methods like loans or venture capital.

Thanks to the success of platforms like GoFundMe and Kickstarter, crowdfunding is steadily on the rise. The market is expected to grow by $196.36 billion in the next 4-5 years, with a 13.86% growth in 2021 alone.

Source: P.R. Newswire

There’s a big opportunity here, as the market currently comprises only several (although well-established) players. The key to success here is to find an underserved niche and tackle it.

For instance, Patreon carved its own space by serving artists and the creative community. On the other hand, Mightycause focused solely on nonprofits. So long as you find your market, the crowdfunding niche can be highly profitable.

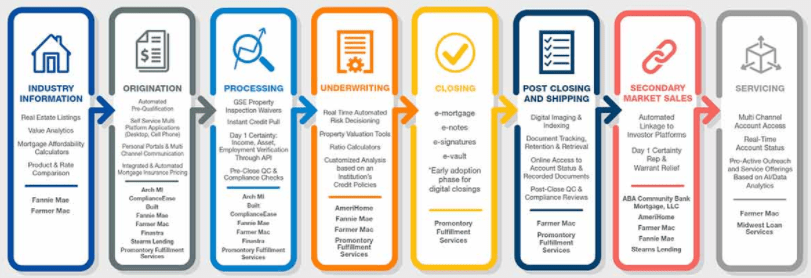

E-mortgage app

Mortgage apps help homeowners streamline the entire home loan application process, from lead generation to closing.

It’s a huge niche, with lots of subcategories that you could specialize in.

Here’s an overview of the digital mortgage process. Each part of that process is ripe for innovation and app development.

Source: American Bankers Association

E-mortgage can also be profitable because the mortgage industry itself is lucrative. But it’s also competitive, as mortgages comprise the largest portion of the U.S. lending sector.

Thus, lenders are always looking for a way to stand out.

Numbers are also proving the effectiveness of e-mortgages. According to a study by Freddie Mac, digital mortgages have shortened loan application times by up to 6 days.

People are welcoming the switch to online mortgage applications, too. ICE Mortgage Technology found that 61% of all borrowers have applied and completed their application via an online portal.

The combination of high demand, underserved sectors, and a lucrative market make e-mortgage an attractive fintech niche overall.

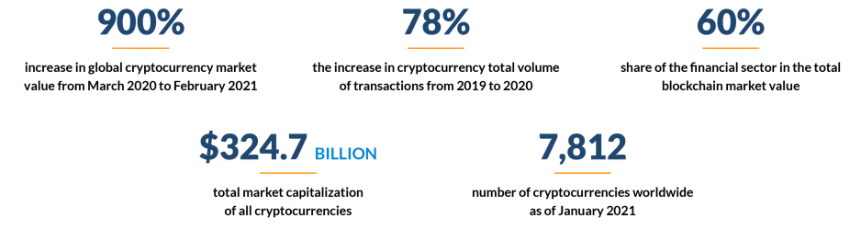

Crypto trading app

Cryptocurrencies have exploded in popularity in recent years, with assets like Bitcoin and Ethereum leading the charge. It’s now a $324.7 billion market comprising over 7,812 different cryptocurrencies.

Source: Finances Online

No wonder crypto trading apps are also on the rise. Many investment apps already on the market like Robinhood and eToro offer crypto trading on top of the usual stock trading.

Additionally, some apps specialize solely in buying cryptos, such as Coinbase and Kraken.

If you’re fascinated by the crypto market and want to capitalize on its popularity, developing a crypto trading app might be worth your while.

However, remember that cryptocurrencies can be complex, so make sure you know them inside and out before developing your app.

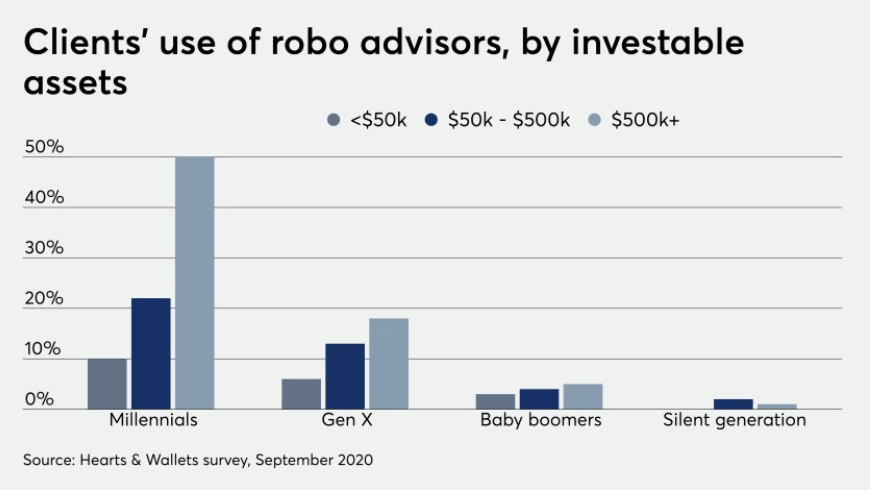

Robo advising app

Robo advisors are essentially digital brokers that automatically manage a part of your portfolio or all of it.

All you need to do is provide your financial goals, current financial standing, and risk appetite. Once done, the algorithm will determine the best investments to help you meet those goals.

The main target of robo advisors is mostly younger millennials who might not be used to working with a financial advisor or broker.

This observation was confirmed by a Hearts and Wallets survey in 2020:

Source: Financial Planning

The biggest advantage of robo advisors is that they can offer the expertise and services of a human advisor at a fraction of the cost. So they’re great for people who want to grow their money but don’t want to manage it actively.

Developing a robo advisor is a great way to help everyday people grow their wealth through investments. That alone makes it a fantastic niche to pick.

Stock trading app

Stocks are by far the most popular financial assets people trade in the markets, as they’re a tested financial instrument and will be around for a long time.

So if you want to develop an investing app with staying power, focusing on stocks might be a good move.

Unfortunately, there’s no shortage of stock trading apps available, which can make it tough to break into this niche. Nevertheless, certain strategies can make you stand out from the crowd.

The most important thing here is education. We all know that investing is risky.

Ensuring that users understand the risks before investing their money can help them avoid unnecessary losses.

Educating them can be done through onboarding or providing learning resources, which is what Wealthfront does.

Source: Wealthfront

You should also have more safeguards in place, more so than any other app. For instance, enforcing limits so that losses can be controlled is a good idea.

And finally, your stock trading app should be transparent. Disclose everything and don’t make any over-the-top claims and promises of guaranteed ROI.

The truth is that stock trading is profitable but risky. So should you choose this fintech niche, focusing on a safe user experience is the way to go.

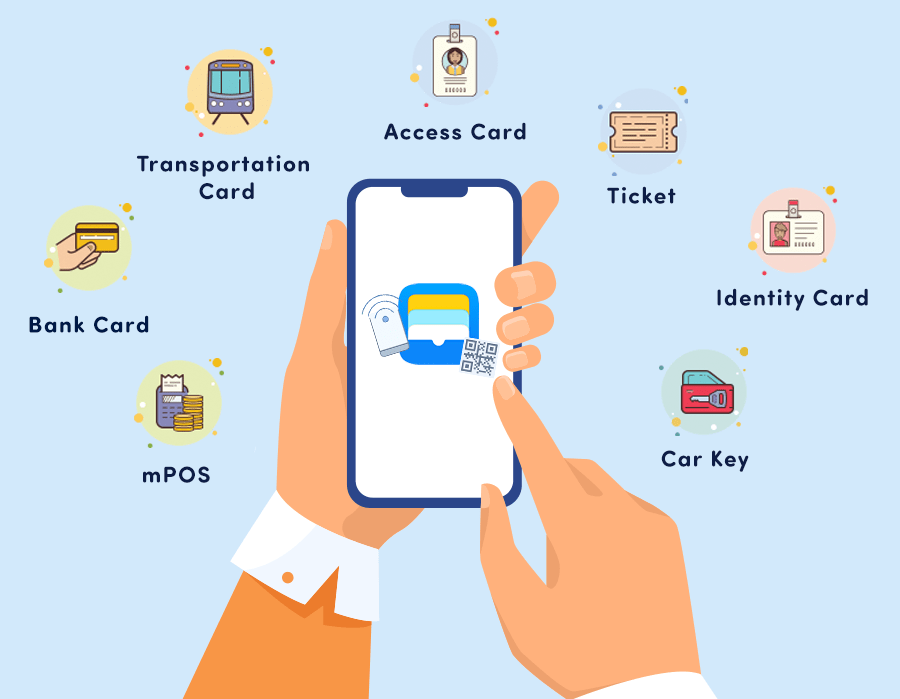

Digital wallet app

A digital wallet is just what it sounds like—a place where you can store all of your digital payment methods.

This includes debit and credit cards, but they can also store tickets and vouchers. Some wallets, like Huawei Pay, even allow you to add digital door keys.

Source: The Paypers

They’re incredibly convenient for cashless payments because you don’t need to remember a dozen credit card numbers or bank accounts. Instead, a simple swipe will do it.

You can also use digital wallets to pay in physical stores through Q.R. code terminals.

The market for digital wallets is huge, and it’s only going stronger thanks to the recent pandemic. A 2021 report predicted that by 2025, more than half of the world’s population would be using mobile wallets.

And as the world continues to digitize, mobile wallets will always stay relevant. That makes it a solid bet for fintech app development.

Financial record maintenance app

Accounting software is nothing new; such solutions have been around since computers became widely available to consumers.

But the innovation offered by financial record maintenance apps is that they make the process much more streamlined and efficient. They also enable entrepreneurs to manage their books anywhere they go by storing data in the cloud.

For instance, accounting apps like Wave allow users to take photos of receipts, making recording expenses fast and straightforward. More comprehensive solutions like Square also offer inventory management and robust reporting on top of accounting.

Financial recording apps are a good niche because businesses will always need them.

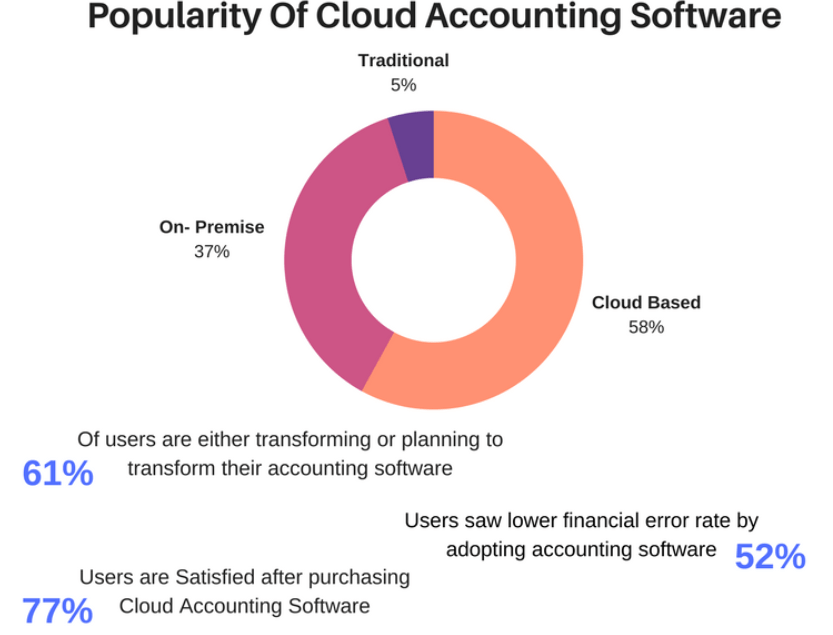

Plus, there’s a steady stream of entrepreneurs who are seeing incredible results since they’ve switched to cloud accounting software, as this survey shows:

Source: Software Suggest

So if you’re planning to pick this niche as your main fintech idea, there’s plenty of momentum and demand to get you through.

Got your fintech app idea down?

Good! You’ve already tackled one of the hardest steps in creating a successful fintech app.

But here comes another obstacle: fleshing out and bringing your idea to life.

Fortunately, there’s no shortage of resources to help you out here. In fact, we have written an excellent primer on building a fintech app.

But if you don’t want to do it all by yourself, you can get our expert assistance. So whichever fintech app idea you have in mind, we think our experience and knowledge can steer you in the right direction.

Contact us today, and let’s get started!