7 Things to consider before building fintech products

So before going any further with your Fintech project, here are seven things you have to consider first.

The COVID-19 pandemic will undoubtedly be remembered as a time of struggle and personal turmoil for many around the globe. Still, one can’t deny that it also spurred a lot of positive, ground-breaking changes.

Take financial technology or FinTech.

Thanks to social distancing and year-long lockdowns, people have embraced contactless payment and digital banking apps in their everyday lives.

It’s no surprise then that FinTech grew an average of 13% at the height of the pandemic, according to a 2020 joint study by the World Bank and the University of Cambridge.

The signs couldn’t be any clearer. If you’re a financial institution or offer financial services, adopting FinTech isn’t a matter of if but when.

And the right time is right now!

Here’s what you need to know when creating a future-ready FinTech app.

The challenge with Fintech apps is that they have to combine user-friendliness, speed, and robust security.

After all, we’re talking about people’s money here.

With that in mind, here are some of the features that every FinTech app must have.

Biometrics refers to security systems that use an individual’s physical characteristics to either grant or deny entry to an app.

In smartphones, this can either be through fingerprint scanning or facial recognition.

Using biometrics solves a long-standing cybersecurity concern—passwords are notoriously unreliable.

Consider that up to 61% of data breaches occur through password hacks, according to Verizon’s 2021 Data Breach Investigations Report.

It all comes down to human nature. People often mismanage or misplace passwords. Worse, many come up with passwords that are easy to guess.

In comparison, biometric security is incredibly secure and almost impossible to bypass.

At the same time, it’s also much more convenient and faster because users don’t need to type in and remember passwords to access the app.

For developers, biometrics are relatively easy to implement. Apple, for instance, provides a robust API for implementing Face ID in any iOS app.

The key with biometrics is to know when to use it.

For example, it’s a good practice to require authentication when a user needs to perform sensitive operations, such as transferring funds or making payments.

Nevertheless, don’t overdo it to the point of inconvenience.

It’s also good practice to provide alternative authentication options if the biometric system fails due to legitimate reasons.

For example, facial recognition might not work when a person is wearing a face mask, so the app should ask for a password instead.

Of course, even something as secure as biometrics is best combined with other security layers to make the app even more robust.

That’s where two-factor authentication (2FA) comes in.

Two-factor authentication (2FA) is one of the more secure and prevalent security methods online today.

To log in with 2FA, you need two types of credentials (hence the name).

One is something that you already know, such as a password.

The other is a passcode generated from a physical device that only you have, such as your smartphone or a USB hardware key.

2FA is secure because, apart from your password, hackers would also need to get hold of your physical device to get to your data.

The passcode that this device supplies changes frequently, so it’s impossible to guess.

Combine that with another security layer like biometrics, and data breaches become next to impossible.

Indeed, a separate study by both Microsoft and Google concluded that 2FA stops up to 100% of automated cyberattacks.

One of the drawbacks of 2FA is that, unlike biometrics, it’s an extra step that can inconvenience some users. They also need to spend time setting it up.

To make it easier for users, you can adopt push notification-based 2FA instead of the traditional method of entering a passcode.

2FA is also not completely infallible.

While it can’t be bypassed directly, hackers can use phishing or social engineering to trick users into revealing their 2FA passcode. SMS-based 2FA also has a potential vulnerability.

If a hacker gets ahold of a user’s phone number with a takeover fraud, they can also hack into the app with a simple password reset.

Blockchain is a decentralized ledger that can log transactions autonomously and anonymously without a third-party entity.

Any data entered on a blockchain is permanent and can never be altered.

The nature of blockchain technology makes it especially attractive for a FinTech app.

Every transaction and money transfer is permanently logged into the ledger, giving your data transparency and fraud immunity.

Unlike your bank account that a financial institution manages, no intermediary maintains the blockchain.

Thus, transactions are faster, cheaper, and more secure. To top it all off, the blockchain is decentralized and distributed to multiple servers, making downtime nearly impossible.

The bottom line is this: blockchain offers a much more secure and transparent way to store and record sensitive financial data.

Given that large financial institutions have proved time and time again that they’re not as reliable as people think, it’s no wonder blockchain is becoming an attractive solution for the finance sector.

There are many ways to implement blockchain in various financial apps beyond recording transactions.

For example, some banks are testing a blockchain-based identity system to prevent fraud.

The technology also facilitates cheaper cross-border payments, which is helpful if your FinTech app targets multiple countries.

Of course, blockchain is still a relatively new technology, so it’s best to do further research and check local regulations.

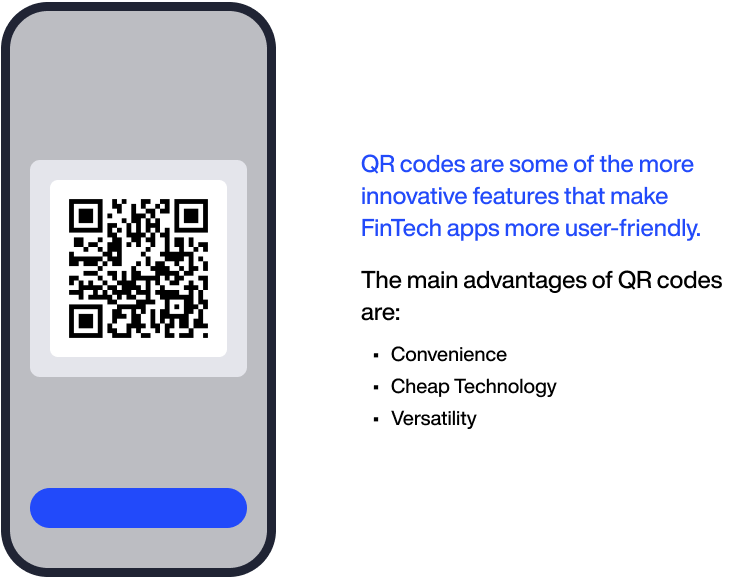

QR codes are some of the more innovative features that make FinTech apps more user-friendly.

It allows users to make app transactions by scanning the code instead of manually entering payment details.

QR scanning is quickly becoming the preferred way to make mobile payments.

According to Juniper Research, close to 29% of mobile phone users globally will use QR codes in making payments by 2025.

In fact, credit card giant Visa has entered the QR game by introducing mVisa in Kenya.

This free service allows mobile phone users to pay directly from their bank account by scanning merchant QR codes. It proved to be a hit, spreading to other countries and spurring MasterCard to develop a rival QR system.

The main advantage of QR codes is convenience.

Users need only scan to make payments; there’s no need to whip out their credit cards from their wallets.

Contactless payment through QR codes was especially vital during the pandemic.

QR codes are also advantageous for app developers.

For one, the technology is cheap. You don’t need any additional equipment to implement QR codes as they will work on-screen or printed. It’s also easy to integrate QR code functionality into any app.

However, you’re not limited to transactions with QR codes.

You can also expand their use to other operations like quickly linking a user’s bank account and other financial services to your app.

There are so many uses for QR code tech that there’s little reason not to implement it on your next FinTech app.

Giving users an overview of their financial transactions through data analytics is helpful in any FinTech app.

People need data to make intelligent financial decisions, which is vital in investment and personal banking niches.

At the minimum, apps should have a reporting feature that allows users to get an overview of their transactions for a given timeframe.

For example, if you have a banking app, it must be easy for someone to check their deposits, withdrawals, and payments per month.

The key to data analytics is simplicity.

Understanding financial data is difficult enough, so it must be presented in a way that’s easy to digest and analyze, even for a newbie.

Visuals like graphs and charts are essential here. Your app can even use AI to give helpful suggestions or recommendations.

At the same time, data analytics must also be flexible.

Users should have the freedom to customize reports and data tracking.

One example includes reporting transactions only from a specific spending category in a personal finance app.

When users feel that they’re in control of their financial data at all times, it’ll make your FinTech app much more usable.

In many ways, building a FinTech app isn’t that different from any other app. There are just a few key steps that you need to consider.

FinTech is such a broad field that there are more than a dozen subsets you can consider. Additionally, more trends are coming in that will disrupt the industry and create even more niches.

Hence, your first decision is to sift through the clutter and pick which niche you’d like to focus on.

Rather than decide on a whim, it’s best to rely on solid market research to guide your choice.

Doing this is important because while some FinTech niches can be profitable, they can also be very competitive.

For instance, the P2P payment sector might be experiencing explosive growth, but it’s currently dominated by established players like Google Pay, Venmo, and Zelle.

Market research will tell you whether entering this niche is a good idea and, if so, how best to do it.

As we’ve explained in a previous article, thorough market research starts with asking the big question: what’s the problem of people in this niche that my FinTech app is trying to solve?

This will inevitably lead you to other questions like:

There are many ways to answer these questions, and they form the core methods of market research.

You can gather data from your target market through surveys, questionnaires, and interviews.

You can also supplement these with competitor research or studies from third-party firms.

If you don’t know where to start, there are plenty of potentially profitable but yet underserved FinTech niches you can explore.

These include lending, insurance tech, and crowdfunding.

Complying with all legal requirements and financial laws is one of the key differences between developing a FinTech app and any other type of software.

Understandably, most governments are especially strict when it comes to services that deal with people’s money.

Compliance should be your top priority because disregarding it can single-handedly bring your entire FinTech operation to its knees.

This is what led the U.S. Federal Trade Commission (FTC) to shut down Blue Global, LLC for unlawfully sharing personal financial data in their lending platforms.

The key to compliance is to get it out of the way as early as possible. Doing this ensures you avoid expensive fines while streamlining the development process.

The first step is to know the regulations governing FinTech in your country. Depending on which area of FinTech you’re dealing with, this can be several.

For instance, in the U.S., credit card transactions are covered by the Electronic Fund Transfer Act (EFTA) of the Federal Reserve Board.

Crowdfunding, meanwhile, is handled by the Jumpstart Our Business Startups Act (JOBS) of the Securities and Exchange Commission (SEC).

Hence, if you plan to launch a peer-to-peer crowdfunding app, you’d need to comply with these two laws.

You’ll quickly realize that legal compliance can be very complicated, tedious, and confusing.

Moreover, it can evolve into a regulatory nightmare if you’re launching a FinTech app in multiple countries with various laws.

Thus, it’s best to hire a lawyer that has experience in handling compliance for FinTech startups.

You can also use regulatory technology (itself a FinTech niche) to automate parts of your compliance process.

Given the sensitive nature of FinTech, it’s crucial that you take extra care in choosing which technologies to use in development.

Using the wrong platform, programming language, or third-party tool can negatively impact your app’s security, scalability, and even performance.

How you pick your technology stack will depend on several factors, but it all comes down to your project’s scope and goals:

These questions can help guide which third-party tools and solutions are suitable for you.

Of course, security is still the most critical consideration. A small security hole in your app is all it takes for a hacker to get in and steal customer data.

Knowing the vulnerabilities of the different programming languages is vital to anticipate these flaws during development.

Scalability is also a key concern.

Your app system and third-party libraries should be able to handle a substantial load of users without any slowdown in performance.

Also, look into the fault tolerance capabilities of the tools you use; even when it encounters an error, it shouldn’t bring down the entire system.

To get you started, here are some of the more popular FinTech technologies.

Python is undoubtedly the most popular programming language for FinTech. It’s easy to use with an extensive open-source library, making it ideal for fast development and deployment.

It’s also highly scalable, making it a flexible language overall.

Java is a traditional language used by financial institutions. Its main advantage is excellent security and cross-platform interoperability.

For apps that require advanced financial computations and concurrent operations, C++ is the best choice.

When it comes to databases, some of the more commonly used in the financial industry are Oracle and DB2.

Both are noted for their high performance, backup features, fault tolerance, and tight security.

Picking out the right technology tools is just one part of FinTech app development. The other part is getting the right team to use these tools successfully.

However, hiring a typical mobile app developer isn’t going to cut it here.

FinTech has specific architecture and compliance requirements that make it an altogether different beast.

Therefore, it would be best to get experienced programmers and engineers who have already taken part in creating a successful FinTech app.

Having at least one cybersecurity expert on your team is also crucial. They can boost your app’s security and help deal with data breaches when they happen.

Of course, you can skip assembling an internal team yourself and just partner with a reputable company with FinTech expertise.

It just so happens that our team at DECODE fits the bill.

We recently partnered with Asseco SEE to develop a cross-platform mobile banking solution that offered a myriad of features, from a mobile wallet to currency exchange.

It was a complex project that required the latest technologies and our combined expertise—and we delivered with flying colors.

When it comes down to it, the secret to success with a FinTech app is collaborating with the right people.

An API (application programming interface) is the set of functions that allows applications to communicate with each other.

The best example is the API that enables a mobile app (the front-end) to send and receive data from the server (the back-end).

In FinTech apps, most core functions also use APIs to connect with third-party servers and resources.

For instance, a mobile banking app needs to interface with the customer’s bank API for their account balance.

Payment apps also need to integrate with other payment providers like Stripe.

When developing your app, building APIs helps streamline the process.

For example, API for core functions like payments or fund transfers can be written once, then reused whenever it’s needed.

You can even extend your APIs to other apps that need the same capabilities, speeding up the development time on future projects.

There are many approaches to API development, but one of the best is RESTFUL API.

This modularized architecture strictly separates the mobile app client from the back-end server that does the bulk of the data processing.

Such layering is exceptionally suited to FinTech thanks to its high security, portability, and scalability.

By now, you already know that security is vital with FinTech apps. However, tight security shouldn’t be limited to just the app itself.

Protection of the entire infrastructure, from the back-end server to the network hosting it, must be prioritized at all costs.

It makes sense when you realize that the bulk of your customer’s data isn’t on their devices but on your servers.

Consequently, a hack on your back-end will cause a leak, no matter how tight your mobile app is.

Worse, a compromised server can act as a backdoor to your users’ devices via your app!

Ensuring infrastructural security involves a combination of robust cybersecurity solutions and strict protocols.

Start by securing your network perimeter and endpoints with next-gen firewalls and proxy servers.

Next, secure all computers and devices connected to your network.

Keep the OS updated on all your devices to resolve any security flaws and vulnerabilities.

Then, protect them with anti-virus software to keep viruses and malware out.

Be wary of any third-party APIs or open-source libraries that you use, as any flaws can compromise the rest of your system.

It’s one of the reasons why you should only get third-party tools from trusted sources.

And whatever you do, don’t install anything on your web server other than what’s necessary. This helps minimize the introduction of security flaws.

Remember that your security is only as strong as your weakest link, so make sure to leave nothing unprotected.

When in doubt, it’s best to hire a cybersecurity consultant to strengthen your defenses.

Like with any other mobile app, a thorough software testing regimen on your FinTech app is crucial.

In a mission-critical industry like finance, even a tiny bug can lead to millions of dollars in losses and lawsuits.

The testing techniques you’ll use with FinTech apps will be roughly the same with other software projects, albeit understandably much more thorough and intense.

Functional testing techniques, for instance, take on a higher level of importance.

That’s because QA testers need to ensure that all app functions are dealing with sensitive financial data and transactions properly and securely.

As a result, more test cases are often required to put the system against every possible scenario.

Performance testing is also crucial with FinTech apps.

Most financial services can’t afford to suffer downtimes, especially when dealing with large volumes of transactions.

Techniques like stress testing and scalability testing can help QA catch performance issues that need to be optimized.

And, of course, there’s security testing.

This often involves ethical hacking techniques like penetration testing, which can effectively simulate how a hacker would exploit vulnerabilities in the system.

With rapid growth and exciting innovations coming in, there’s no better time to get into the FinTech game. It’s an industry that will revolutionize finance unlike any other.

Of course, there are plenty of challenges, just as there are opportunities. With the right app idea and a reputable collaborator, you too can achieve FinTech app success.

We hope we’ve inspired you to develop a FinTech app. If you want to learn more about FinTech, read our other article here.

A seasoned software engineering executive, Marin’s role combines his in-depth understanding of software engineering processes (particularly mobile) with product and business strategies. Humbly boasting 20+ years of international experience at the forefront of telecoms, Marin knows how to create and deliver state of the art software products to businesses of all sizes. Plus, his skills as a lifelong basketball player mean he can lead a team to victory. When he’s not hopping from meeting to meeting, you’ll find Marin listening to indie rock, or scouring the latest IT news.

So before going any further with your Fintech project, here are seven things you have to consider first.

Everything you need to know about 2021 fintech mobile app trends, opportunities, and regulations in this exciting time for personal finance innovation

We’re more than a tightknit team of skilled developers — we’re partners and visionaries helping you realize your goals.